Volatility has reigned supreme on Wall Street for the past four years. The three major stock indexes have oscillated between bear and bull markets since 2020.

In times of turbulence, investors gravitate towards tried-and-true stalwarts. While the “FAANG stocks” have been the go-to for investors since 2013, the “Magnificent Seven” are now commanding the spotlight.

Image source: Getty Images.

A Magnet for Investors: The Magnificent Seven Stocks

By “Magnificent Seven”, I’m referring to:

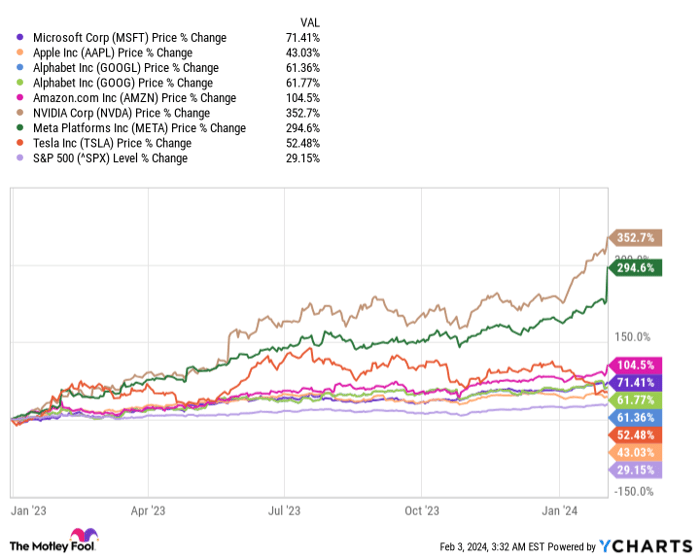

These seven industry leaders have significantly outperformed the benchmark S&P 500 since the start of 2023. Each boasts sustained competitive advantages, drawing investors keen on their long-term appeal.

- Microsoft’s Windows remains the undisputed leader in desktop operating systems, and Azure ranks second in global cloud infrastructure services market share.

- Apple’s iPhone has dominated the domestic smartphone market for over a decade, and its capital-return program towers over all other public companies.

- Alphabet’s Google holds a commanding 91.5% of the global internet search share, and is the parent of YouTube and Google Cloud.

- Amazon accounts for nearly 40% of all U.S. online retail sales and owns Amazon Web Services, a key player in cloud infrastructure services.

- Nvidia’s A100 and H100 GPUs are set to capture around 90% of AI-inspired GPUs deployed in high-compute data centers in 2024.

- Meta Platforms boasts the top social media real estate with Facebook, Instagram, WhatsApp, and Facebook Messenger, collectively drawing nearly 4 billion users each month.

- Tesla leads in North America’s electric-vehicle market, with almost 1.85 million EVs produced in 2023 and driving recurring profits.

Although the Magnificent Seven outperformed in 2023, their prospects for 2024 and beyond vary significantly. As we step into the shortest month of the year, one stock appears undervalued, while another flashes warning signals.

A Diamond in the Rough: Alphabet

Among the seven behemoths that make up the Magnificent Seven, Alphabet stands out as the most enticing investment at present.

While most of the Magnificent Seven performed well in earnings, Alphabet took a hit, particularly in its core advertising segments.

Much of the concern for Alphabet revolves around the fact that a sizeable 76% of its $86.3 billion total revenue in 2023 came from advertising. Advertising spending is known to contract at the faintest indication of economic unease in the U.S. or globally. Certain monetary measures and indicators hint at an impending downturn in the U.S. economy in 2024.

However, it’s crucial for investors to maintain perspective. History unequivocally shows that recessions are usually short-lived. Of the 12 recessions since 1945, nine have ended within a year, with none extending beyond 18 months. Conversely, periods of expansion have been known to endure for years. Investing in ad-driven leaders during brief economic slumps has historically proven to be a shrewd move.

Alphabet remains an exciting prospect due to its unassailable position in the advertising sphere. Google holds an astounding 91.5% of the global internet search share. Such an overwhelming share has been uninterrupted for nearly nine years, granting Alphabet unmatched pricing leverage for advertisements.

Unraveling the Financial Future of Alphabet and Nvidia

The Bright Future of Alphabet: Embracing New Revenue Streams

Alphabet, the parent company of Google, is poised for an impressive financial updraft, largely driven by its ancillary operating segments. A striking surge from 6.5 billion in 2021 to over 50 billion daily views of YouTube Shorts by last year is propelling formidable momentum. This new monetization channel has significantly bolstered YouTube’s ad revenue, painting a rosy picture for upcoming earnings.

Moreover, Google Cloud recently marked its fourth consecutive quarter of operating income after enduring years of operating losses. The nascent stage of enterprise cloud spending hints at a double-digit, exceptionally high-margin growth outlook for the company’s cloud infrastructure services, creating a fertile ground for revenue expansion.

The allure of Alphabet’s appeal is further amplified by its attractively low valuation. Surprisingly, its forward price-to-earnings (P/E) ratio of 18 is below the S&P 500’s forward P/E, despite Alphabet’s superior growth rate. Furthermore, with a valuation of less than 13 times the forward-year cash flow, compared to an average of 18 times over the past five years, Alphabet’s stock emerges as a compelling opportunity. Bolstering its attractiveness is a substantial $97.7 billion net cash buffer, establishing it as a compelling investment prospect for February and beyond.

Image source: Getty Images.

Avoiding Nvidia: A Cautionary Tale

Conversely, within the realm of prosperous stocks, semiconductor giant Nvidia’s shine is losing its luster, urging investors to exercise caution in February and beyond. Nvidia’s prowess in AI solutions, exemplified by the soaring popularity of its A100 and H100 GPUs, has been an integral part of its narrative. However, the company’s ongoing success faces potential hurdles, predominantly arising from overproduction and competitive encroachment.

An upsurge in output of A100 and H100 GPUs, facilitated by Taiwan Semiconductor Manufacturing, may lead to a decline in Nvidia’s gross margin in fiscal 2025. The potential saturation of the market for GPUs used by AI-accelerated data centers, compounded by strong competition from Advanced Micro Devices and Intel, further clouds Nvidia’s future profitability.

Regulatory constraints add salt to Nvidia’s wounds, with export restrictions placed on its chips destined for China, presenting a perilous threat to its sales revenues. Challenging the inevitability of AI’s dominance, historical investment trends suggest a wavering future, raising skepticism about the sustainability of Nvidia’s growth trajectory.

At more than 61 times estimated cash flow in fiscal 2024, Nvidia’s laundry list of red flags renders it a clear contender for avoidance in February, urging investors to approach with a discerning eye.

Assessing Alphabet’s Investment Potential

Should you invest $1,000 in Alphabet right now?

Before considering an investment in Alphabet, heed this advice:

The Motley Fool Stock Advisor recently unveiled its extensive research uncovering the 10 best stocks for potential investors, with Alphabet conspicuously absent from the roster. The handpicked 10 stocks are anticipated to yield substantial returns in the foreseeable future.

Embracing investors with a roadmap to success, the Stock Advisor service offers invaluable guidance, including portfolio-building strategies, regular analyst updates, and two new stock recommendations each month. The service has profoundly outperformed the S&P 500 since 2002, indicative of its prowess in delivering impactful investment insights*

*Stock Advisor returns as of January 29, 2024

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.