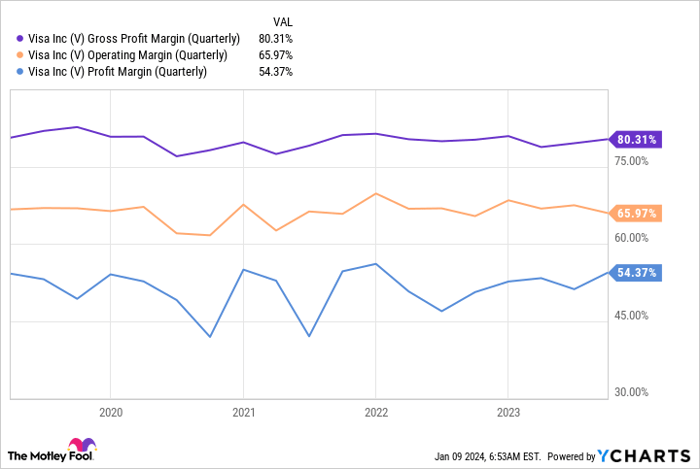

The Visa Verdict

Buffett adores businesses that operate like toll booths. The model is straightforward: Develop an infrastructure and pocket a portion of the revenue from everything that flows through it. Visa’s payment processing structure is one of the greatest toll-booth model businesses in history.

Every time a Visa-branded card is swiped, the company collects a small usage fee, leading to substantial profits. Even more impressive, Visa consistently boasts some of the highest profit margins of any enterprise.

Few companies have the ability to transform over half of their revenue into net profit, but Visa achieves this feat. Furthermore, despite its massive scale, Visa continues to achieve robust growth. In the company’s fourth quarter of fiscal 2023, revenue surged 11% to $8.6 billion, establishing a new record high.

Despite its exceptional business model and impressive upward momentum, Visa trades at only 32 times trailing earnings and 27 times forward earnings — some of the most favorable levels seen in the past five years. This presents a compelling buying opportunity, especially from a long-term perspective.

The Amazon Advantage

Berkshire may not hold a significant stake in Amazon, but the stock is a prime buy at the moment. Under the leadership of CEO Andy Jassy, Amazon’s business has undergone a remarkable upturn, exhibiting consistent and escalating profitability. The company’s renewed focus on enhancing its bottom line became evident in 2023.

Amazon’s revenue growth has also rebounded, surging 13% in the third quarter. Amazon is firing on all cylinders right now, and even though Berkshire Hathaway trimmed its position in Q3, Amazon emerges as a fantastic buy at present.

The Apple Anomaly

Apple is unequivocally Buffett’s and Berkshire’s favorite stock, constituting nearly half of the portfolio at around 47%. However, this heavy concentration could pose a problem in 2024.

While Apple’s stock performed admirably in 2023, posting a 48% gain, the business grappled with declining revenue throughout the fiscal year. This downturn extended across all product lines. When a company experiences operational challenges, yet its stock remains stagnant or climbs, this signals an excess of optimism. Although Apple might not be in a bubble just yet, it is valued at 32 times trailing earnings and 29 times forward earnings estimates — a steep price for a contracting company.

Despite being Berkshire’s top pick, Apple is far from a prudent buy at the moment. In contrast, the other two companies mentioned are in a much stronger position than Apple, making them more attractive options for investors pondering Berkshire-owned stocks.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.