As the second quarter earnings season draws to a close, it’s time to reflect on the performance of companies and the overall market. Most companies have reported growth in both revenue and earnings per share (EPS), with a commendable 10.9% increase in EPS across the board.

Despite the market’s early August volatility, the S&P 500 stands resilient, showcasing a nearly 3% return over the past two months.

Optimism prevails in the macroeconomic landscape, with concerns arising from a slight labor market softening, especially after the Bureau of Labor Statistics’ recent downward revision.

Currently, the recession likelihood hovers at a modest 20%, a figure ascertained by Goldman Sachs, portraying a bearable risk level for this stage of the economic cycle.

With these parameters in mind, let’s delve into three crucial takeaways from this earnings period.

Rejuvenated Bulls in the Earnings Arena

The outlook for the second quarter of 2024 remains promising. FactSet data reveals that 79% of companies have outperformed EPS forecasts, while 60% have exceeded revenue projections.

These percentages surpass the 5-year and 10-year averages of 77% and 74%, respectively. Notably, this earnings season has seen companies surpass these averages by 0.8 percentage points in revenue and an impressive 3.9 percentage points in EPS. Noteworthy sectors like financial institutions and utilities have particularly shone in their results.

Within the U.S., a resilient consumer landscape prevails, as evidenced by reports from major retailers like Walmart indicating robust consumer spending across various income brackets. Nevertheless, caution echoes from companies such as McDonald’s and PepsiCo, signaling a discerning consumer base amidst prolonged high inflation and economic uncertainty.

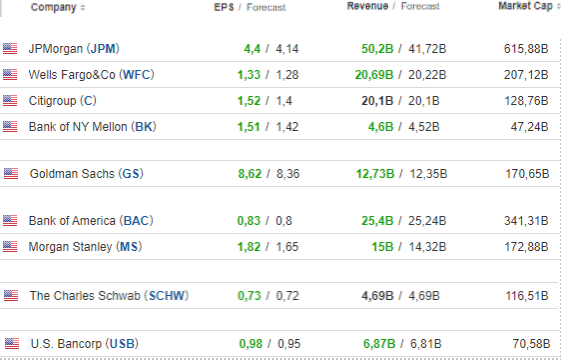

Potential Uplift for Financial Sector via Rate Cuts

During the interest rate elevation phase, the financial sector benefited from augmented interest income, primarily driven by expanded lending activities.

However, with the cost of maintaining deposits starting to dent earnings, industry representatives eagerly await potential rate cuts, potentially kickstarting at the upcoming September meeting.

The finance industry basked in a noteworthy 17.6% year-on-year profit growth, securing the third position in terms of profit expansion across diverse sectors.

Bolstered by overall satisfactory outcomes from recent stress tests conducted on banks, a comprehensive pivot by the Federal Reserve may further uplift the industry’s encouraging performance in forthcoming quarters.

Big Tech’s Dilemma: Overspending in AI?

The tech behemoths’ substantial investments in artificial intelligence are stirring concerns. With the intelligence race heating up, companies are pumping substantial capital into this domain. For instance, Alphabet, despite surpassing earnings estimates, saw its stock plummet by nearly 5% following news of a hefty $13 billion investment in upgrades. Google’s capital expenditure surged by a staggering 91% year-on-year during the second quarter.

Next week, all eyes will be on Nvidia’s quarterly report release scheduled for Wednesday. The market’s optimism prevails, evident in numerous upwards revisions in forecasts.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.