Familiar with the age-old wisdom on 401(k) wealth-building? It’s akin to hearing your granny’s advice on saving pennies – ever-reliable and unassailably sound:

- Max out those 401(k) contributions religiously.

- Don’t leave free money on the table by missing out on the employer match.

- The earlier you start, the better – and never surrender to the temptation to touch your nest egg.

Stubbornly sticking to these tried-and-true rules practically ensures a spot in the coveted 401(k) millionaire club down the line. Yet, did you realize that attaining that million-dollar milestone doesn’t always necessitate pedaling at full throttle?

No siree! You can effortlessly hit that seven-figure mark within your 401(k) nest egg sans the extremities of the sacrosanct principles outlined above. The dirty little secret behind this millionaire-making retirement blueprint? It’s a cakewalk.

So, let’s delve into three nifty methods that could ease your journey to retire wealthy.

Grounded Expectations

Each financial scenario boasts a distinct flavor, making it impossible to address every entanglement here. Yet, setting reasonable benchmarks rooted in national averages is a good place to start. Thus, a 401(k) calculator akin to the nifty CalcXML tool can provide invaluable insights, requiring essential details such as:

- Years left until retirement

- Current balance in your 401(k)

- Current contribution percentage relative to your salary

- Employer’s 401(k) matching policy

- Expected investment returns in and before retirement

- Anticipated retirement fund duration

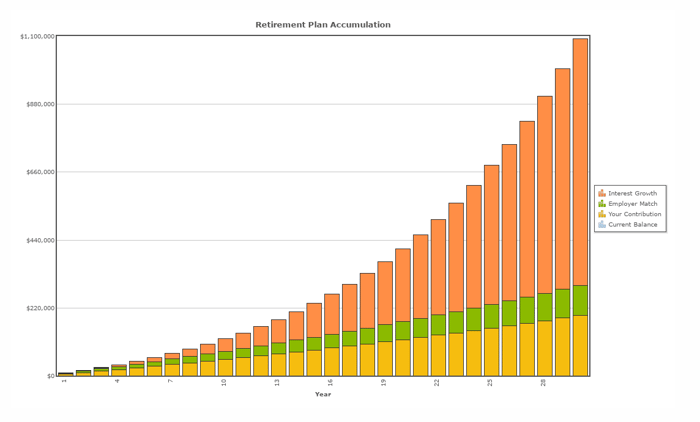

For illustrative purposes, let’s assume a standard scenario featuring three decades until retirement (say, from 35 to 65 years of age), an annual salary pegged at $60,000, incremental salary hikes at a 2% clip, zilch starting funds in the 401(k) coffers, and an 8% contribution to your 401(k) kitty endorsed by a generous 50% employer match (equivalent to 4% of your annual earnings).

These figures closely mirror national averages, erring conservatively. Except where noted, default variables remained unaltered. With an 8% annual returns scenario denoting moderate growth, the final tally stands at $1.1 million in 30 years – a smidgen above the fabled million-dollar threshold.

Chart Source: CalcXML.

1. Time in the Market Trumps All

In this hypothetical scenario, your initial yearly contribution would total $4,800 in 2024, escalating to $6,470 by 2054. Concurrently, employer contributions would start at $2,400, culminating in $3,235 by the final year. Cumulatively, your contributions would near the $300,000 mark.

Interestingly, over two-thirds of your nest egg would stem from investment returns alone.

Even in the modest situation under the moderate 8% average annual growth rate scenario, the S&P 500 index has historically notched an 8.4% compound annual growth rate over three decades fraught with tumultuous market gyrations. Opting to reinvest dividends would have yielded an impressive 10.5% annual return:

Now, considering the extended period, the dividend-enhanced long-term average mirrors the aggressive returns alluded to in the previous example, translating to a near $2 million windfall after three decades. Ergo, achieving the hallowed million-dollar milestone within this timeframe should present no Herculean feat under even the most conservative investment assumptions.

2. Market-Beating Returns Aren’t Always a Necessity

True, amassing wealth could be expedited should your 401(k) scheme permit individual stock selection, with fortuitous picks reaping substantial gains. Think of sailing through financial markets with Apple and Microsoft‘s market-beating stock offerings. More is always merrier, but fret not – you can materialize that million-dollar cocoon over three decades sans any stock-picking stroke of serendipity.

3. ETFs: Simplifying the Pursuit of Market Parity

All it takes is an unpretentious exchange-traded fund (ETF) shadowing a reputable market index, coupled with minimal annual fees.

The Vanguard S&P 500 ETF springs to mind, boasting an almost seamless alignment to the foremost market index’s returns, accompanied by minuscule management expenses and an effortless dividend reinvestment mechanism.

Alternatively, tracking American blue-chip stocks with the Dow Jones Industrial Average ETF Trust proves a safe bet. For bolder investors, the Invesco QQQ Trust, which traces the NASDAQ Composite Index, offers a more spirited alternative to the S&P 500 – frequently outperforming the latter over measured time spans.

Unveiling the Retirement Sacrosanct: A Diverse Array of Market-Index ETFs

The Unseen Opportunities in Market-Index ETFs

For investors longing to dance in the wellsprings of financial market stability, exchange-traded funds (ETFs) like the Vanguard S&P 500 ETF bring forth a tantalizing melody. These ETFs, akin to the Vanguard S&P 500, elegantly mirror the buoyant returns of resilient market indices while humming a tune of minimal annual fees.

Consider these ETFs as a symphony waiting to be conducted—mix and match at your discretion with no discordant notes in sight, as long as you keep your tableau adorned with sturdy, low-fee performers.

The Long-Term Anthem: Your Financial Future

The compass guiding you towards a shore called ‘financial independence’ whispers harmony from the tool above. It sings a refrain with only two chords—robustness and thrift—a melody that can resonate through the corridors of time.

Embrace the solemnity of this financial sonnet and sow the seeds of your 401(k) contributions today. The future symphony of your millionaire self will bow in gratitude for this harmonious prelude.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.