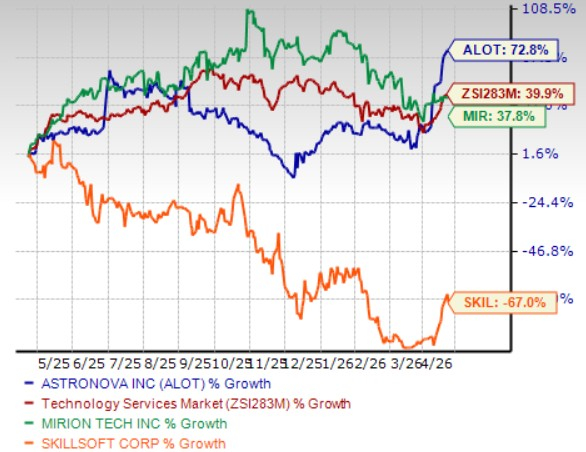

AstroNova, Inc. ALOT shares have surged 72.8% in the past year compared with the industry’s 39.9% growth. The company has outperformed other industry players, including Mirion Technologies, Inc. MIR and Skillsoft Corp. SKIL. Shares of Mirion Technologies have gained 37.8%, while Skillsoft stock has plunged 67% in the same time frame. ALOT benefits from strong aerospace demand recovery, rising aircraft production, growing ToughWriter adoption, improving Product ID performance and high recurring consumables revenues.

Image Source: Zacks Investment Research

A Key Look Into ALOT’s Business Operations

AstroNova designs, develops, manufactures, and distributes specialty printers and data acquisition systems, integrating hardware and software to capture, analyze, and present data across industries such as aerospace, automotive, manufacturing and packaging. Its operations are divided into two segments: Product Identification (Product ID) and Aerospace. Product ID focuses on digital printing systems, supplies, and labeling solutions under brands like QuickLabel and TrojanLabel, serving brand owners and commercial printers. The Aerospace segment provides flight deck printers, networking hardware, and data acquisition systems used in aviation, defense and industrial applications. The company leverages expertise in data visualization technologies, including signal processing and image analysis, supported by in-house manufacturing and global distribution through direct sales and partners.

AstroNova’s Key Tailwinds

A key positive factor for AstroNova is the strengthening demand environment in its Aerospace segment, supported by recovery in aircraft production and utilization. The company continues to benefit from sustained OEM demand as aircraft build rates improve globally. Additionally, the transition toward its ToughWriter product family has been significant, with these printers now accounting for more than 80% of flight deck shipments. This shift improves product mix, enhances margins, and reinforces the company’s positioning in a highly specialized and regulated market.

Another important driver is the ongoing improvement in the Product ID segment. The company has implemented a more focused go-to-market strategy, leveraging analytics to better target high-value applications and customer segments. This has resulted in stronger order momentum and improved customer retention. The focus on regulated verticals such as life sciences, industrial, and chemical markets — where durability and compliance are essential — further strengthens demand visibility and supports long-term growth prospects.

AstroNova also benefits from a substantial base of recurring revenue, particularly within the Product ID business. A large portion of sales is derived from consumables such as labels, inks, and related supplies, which customers must replenish regularly. Around 69% of total revenues is recurring, providing stability and predictability. This recurring nature of revenue helps cushion volatility and ensures a steady stream of cash flows even during uncertain macroeconomic conditions.

Operational efficiency initiatives and cost discipline are further supporting performance. The company has undertaken restructuring efforts, streamlined its product portfolio, and improved productivity across operations. These actions have contributed to margin improvement in the latter half of fiscal 2026. In addition, the expected expiration of a royalty obligation in the Aerospace segment is projected to add approximately $2 million annually to gross profit, creating an additional boost to profitability in upcoming periods.

Lastly, AstroNova’s financial position has strengthened, driven by improved cash generation and debt reduction. The company has enhanced its liquidity profile and reduced leverage, which increases financial flexibility. Stronger operating cash flows and disciplined capital allocation allow the company to invest in growth initiatives while maintaining balance sheet health.

Challenges Persist for ALOT’s Business

AstroNova faces several headwinds that could pressure growth and profitability, including sensitivity to cyclical end markets such as aerospace and industrials, where downturns or slower aircraft production can reduce demand. The company is exposed to supply chain disruptions, reliance on single or limited-source suppliers, and potential cost inflation in components and labor, which can compress margins. Competitive intensity and rapid technological change require continuous innovation, creating execution risk if new products fail to gain traction. Integration challenges from acquisitions like MTEX, along with goodwill impairments and ongoing arbitration disputes, add operational and financial uncertainty.

AstroNova’s Valuation

The company is cheaply priced compared with the industry average. Currently, ALOT is trading at 0.79X trailing 12-month EV/sales value, below the industry’s average of 3.3X. The metric also remains lower than both the company’s peers, Mirion Technologies (5.36X) and Skillsoft (1.03X).

Image Source: Zacks Investment Research

Conclusion

Despite challenges such as cyclical demand exposure, supply chain risks and integration complexities, AstroNova’s strengthening aerospace demand, expanding high-margin product mix, recurring revenue base, and improved operational efficiency position the company for steady long-term growth and profitability.

Strong fundamentals, coupled with ALOT’s undervaluation, present a lucrative opportunity for investors to add the stock to their portfolio.

Beyond Nvidia: AI’s Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren’t likely to keep delivering the biggest profits. Little-known AI firms tackling the world’s biggest problems may be more lucrative in the coming months and years.

Mirion Technologies, Inc. (MIR) : Free Stock Analysis Report

AstroNova, Inc. (ALOT) : Free Stock Analysis Report

Skillsoft Corp. (SKIL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.