Veeva Systems Inc. VEEV continues to benefit from demand for life sciences cloud platforms, with steady progress in Vault CRM migrations and ongoing expansion across R&D and Quality solutions. Management’s fiscal 2027 outlook calls for mid-teens revenue growth and a stable adjusted operating margin, assuming an unchanged macro environment.

The company’s AI roadmap adds an important long-term lever. However, the near-term math remains anchored to the subscription base, not a sudden AI-driven revenues step-up.

VEEV’s Falcon Targets High-Volume Workflow Automation

Falcon is positioned as an agent layer built to take on standardized, high-volume work, with early use cases centered on clinical document intake and safety case processing. That focus matters because those tasks sit at the heart of clinical, regulatory and safety workflows, where repetitive intake and routing can consume significant staff time.

Strategically, Falcon aims to create an automation layer that can scale across multiple functions as Veeva’s footprint broadens beyond its historical commercial roots into clinical development, safety and regulatory operations.

Veeva’s Pricing Models and Adoption Signals

Monetization is still developing. Management has discussed usage-aligned approaches, such as charging per document or per case, but pricing has not been finalized. In practical terms, that creates a wide range of possible outcomes for revenue timing and magnitude, even if the product value proposition is clear.

Falcon remains early, with the company still signing initial agreements and using customer data for quality control and training agents ahead of broader rollout. For investors, the adoption curve is the key variable to watch because early deployments in narrow workflows do not automatically translate into scaled, repeatable revenues.

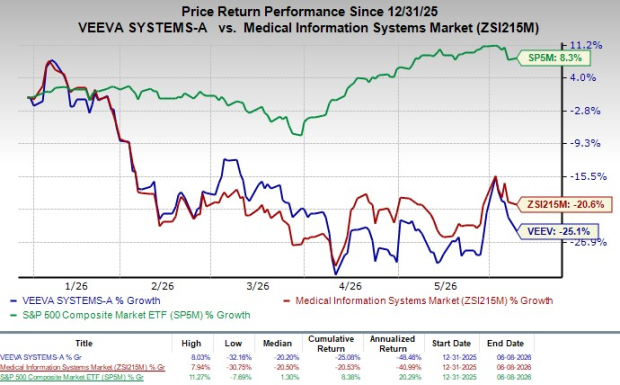

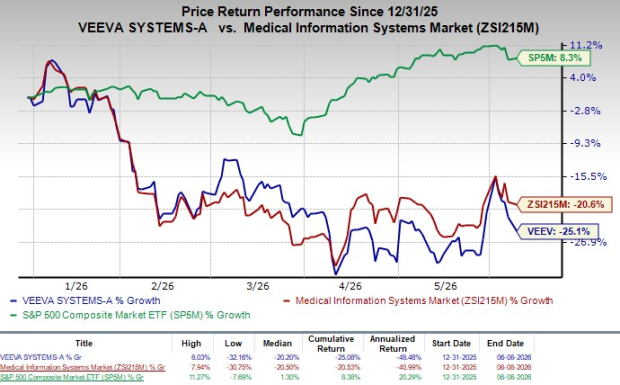

Image Source: Zacks Investment Research

VEEV’s Vault AI Adds Embedded Use Cases

Alongside Falcon, Veeva is scaling Vault AI inside its applications. The emphasis here is on embedded capabilities that automate labor-intensive processes within existing workflows, rather than a standalone agent layer that orchestrates tasks across systems.

Falcon is designed to tackle “agentic” labor in high-volume, standardized work, while Vault AI strengthens the day-to-day utility of the underlying apps customers already use. Over time, both can raise platform stickiness by reinforcing the value of an integrated ecosystem that spans clinical, safety, regulatory, quality and commercial functions.

Veeva’s Near-Term AI Revenues Look Limited

Expectations should stay grounded. Management expects AI revenue to be immaterial in fiscal 2027 outside of Ostro, with the current priority on product quality and customer success. That sequencing keeps near-term financial results tied primarily to execution in the core subscription portfolio.

The investor takeaway is that AI is best viewed as optionality rather than a near-term driver. The focus should be on whether Falcon and Vault AI meaningfully expand workflow value and adoption over time, instead of the amount of revenue generation in fiscal 2027.

Veeva’s Competitive and Execution Risks for AI

Execution risk is real on multiple fronts. CRM decisions remain competitive, and Veeva also faces platform dependencies, including Salesforce for legacy Veeva CRM and Amazon Web Services for Vault-based applications. The prior agreement with Salesforce expired on Sept. 1, 2025, and includes seat-based limits for existing customers during a wind-down period through Sept. 1, 2030, adding complexity to the transition.

For Falcon specifically, uncertainty around the adoption pace and the timing of revenue contribution remains elevated because monetization is not finalized and the rollout is still in early agreements and training. Meanwhile, cost pressures have already weighed on profitability, with gross margin contracting 220 basis points year over year to 74.9% in the fiscal first quarter as infrastructure and services costs rose.

VEEV currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

VEEV’s Milestones to Track Through FY27

Key milestones are practical and measurable. First is a finalized Falcon pricing approach and whether usage-aligned models (per document or per case) translate into repeatable customer agreements. Next is the number and depth of Falcon deployments beyond the initial clinical document and safety intake workflows, along with evidence of tangible workflow impact inside Safety and clinical operations.

On the embedded side, investors should watch Vault AI’s expansion within core applications and whether it improves adoption and retention across the broader platform. Finally, track whether newer product lines such as RTSM, Safety and LIMS continue scaling while management sustains its fiscal 2027 expectation for a stable adjusted operating margin.

For context within the broader Medical Info Systems group, Enovis Corporation ENOV carries a Zacks Rank #2, while Evolent Health, Inc EVH has a Zacks Rank #3 (Hold). That mix underscores how stock performance in the space can diverge based on execution, making Veeva’s migration progress and AI delivery the focal points through fiscal 2027.

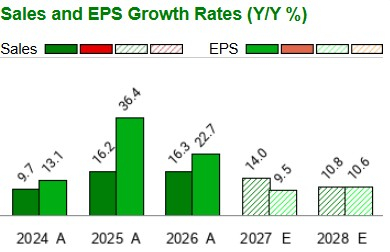

VEEV’s Sales & EPS Picture

In fiscal 2027, VEEV is expected to experience growth of 13.9% in revenues. On the profitability front, earnings per share are expected to improve 9.5% year over year.

Image Source: Zacks Investment Research

VEEV’s Valuation Picture

VEEV currently trades at a price-to-book ratio of 3.79X, well below its industry’s current level of 6.24X.

Image Source: Zacks Investment Research

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

Veeva Systems Inc. (VEEV) : Free Stock Analysis Report

Evolent Health, Inc (EVH) : Free Stock Analysis Report

Enovis Corporation (ENOV) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.