Loyalty Ventures, a prominent player in consumer loyalty and marketing, is facing a critical crossroad. As analysts weigh in on the company's survival, concerns are growing amidst recent challenges.

The stock price decline, driven by factors like inflation, a strong U.S. dollar, and the ongoing pandemic, has raised doubts about Loyalty Ventures' future. Additionally, the loss of a key customer and impairment charges have added to the company's struggles.

In this article, analysts delve into the risks and challenges the company faces in the current market. They explore potential turnaround strategies, the company's valuation, and the potential need for restructuring.

With Loyalty Ventures' fate hanging in the balance, analysts provide valuable insights into its potential survival.

Key Takeaways

- LYLT has faced significant challenges including a decline in stock price, loss of customers, and decline in free cash flow.

- However, there is potential for a turnaround with easing spin-off selling pressure and expected improvements in margins and free cash flow.

- The stock is undervalued and has a potential upside of 512% according to valuation estimates.

- There are risks and challenges, including the perception of AirMiles as a melting ice cube and potential insolvency risk due to debt levels and loan covenants.

Overview of LYLT and Its Challenges

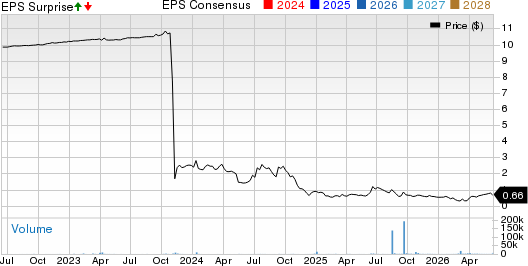

LYLT faces numerous challenges as a tech-based consumer loyalty and marketing company. These challenges include a significant decline in stock value and the loss of key customers. Since its spin-off from Alliance Data in November 2021, LYLT has experienced a decline of over 90% in stock performance. This decline can be attributed to several factors, including the impact of the pandemic on its operating performance. The pandemic has affected LYLT's ability to generate revenue and retain customers, resulting in a downward trend in its stock value.

Additionally, the loss of key customers, such as Sobeys, has had a significant negative impact on LYLT's financial performance. These challenges have contributed to the current struggles faced by LYLT. It highlights the need for strategic measures to address these issues and improve its overall performance.

Potential Turnaround and Valuation

Analysts are cautiously optimistic about the potential turnaround and valuation of Loyalty Ventures, highlighting improvements in key factors such as margins, free cash flow, and normalized earnings. The improving financial performance of the company suggests that it may be able to overcome the challenges it has faced.

Here are three important points to consider:

- Margins: Analysts have observed that the company's margins have the potential to improve, as factors such as inflation and supply chain issues are expected to ease. This could lead to higher profitability.

- Free Cash Flow: The company's ability to generate free cash flow is seen as a positive sign. As the company focuses on growth and potentially replaces lost revenue, the cash flow situation is expected to improve further.

- Market Perception of AirMiles: The perception of AirMiles as a melting ice cube has raised concerns about its sustainability. However, analysts believe that Loyalty Ventures can address these concerns and demonstrate the long-term viability of AirMiles as an independent loyalty program management company.

Risks and Challenges

The risks and challenges faced by Loyalty Ventures include:

- Potential customer attrition and the possibility of a severe recession in 2023.

- Perception concerns regarding the sustainability of AirMiles and the loss of significant partners undermine the perception of AirMiles' success.

- Higher redemption rates compared to issuance also raise doubts about future cash flow.

- The company's caa2 credit rating from Moody's and confidential debt talks suggest potential insolvency risk.

- Breaching loan covenants would have severe implications for the company.

- The potential loss of another partner or a consumer spending recession could lead to further challenges.

- The long-term viability of AirMiles as an independent loyalty program management company is also being questioned, as the commoditization of rewards management may reduce the demand for AirMiles.

Potential Restructuring and Financial Impact

Potentially, a debt restructuring could have a significant financial impact on Loyalty Ventures. The market's expectation of bankruptcy is reflected in the current stock price. Here are three key points to consider regarding the potential restructuring and its financial implications:

- Equity holders may be wiped out: With high debt-to-equity ratios, a debt restructuring could result in the elimination of equity holders' value. The company's ability to turn things around will be influenced by the announcement of new clients and its ability to attract them.

- Uncertainty surrounding the outcome: The outcome of the restructuring remains uncertain. It's unclear if the accumulated miles held in a trust account can be invested in safe assets such as T-Bills. Additionally, the company's high levels of debt, due to ADS's decision, have accelerated the deterioration of its core business.

- Debt covenant challenges: Loyalty Ventures may struggle to meet its debt covenants in 2022. Breaching these covenants would have severe implications for the company. However, it's important to note that the debt doesn't mature until 2026/2027, and the current interest coverage ratio of 3x and debt/EBITDA of 5x provide some breathing room.

Analyst's Position

The analyst holds a beneficial long position in LYLT, indicating their confidence in the company's potential for survival and improvement. Despite the market pricing LYLT for imminent bankruptcy, the analyst believes that the current stock price reflects an overly pessimistic view. The analyst points out that the debt doesn't mature until 2026/2027 and highlights the current interest coverage ratio of 3x and debt/EBITDA of 5x, which suggests that the company has a reasonable ability to meet its debt obligations. Additionally, the analyst attributes the current pricing to selling pressure rather than fundamental weaknesses in the company. Overall, the analyst believes that LYLT could provide considerable gains over time and with improvements in its financial performance.

| Analyst's Position | Market Outlook |

|---|---|

| Beneficial long position in LYLT | Pessimistic, pricing for imminent bankruptcy |

| Debt doesn't mature until 2026/2027 | Reasonable ability to meet debt obligations |

| Current interest coverage ratio of 3x and debt/EBITDA of 5x | Selling pressure contributing to current pricing |

| Confidence in company's potential for survival and improvement | Potential for considerable gains with time and improvement |

Conclusion

Based on the analyst's position and assessment of LYLT's potential for survival and improvement, it's evident that there are considerable opportunities for the company to overcome its current challenges and thrive in the future.

Despite the market's perception of LYLT as being on the brink of bankruptcy, the analyst believes that the company's debt doesn't mature until 2026/2027, and it currently has a decent interest coverage ratio and debt/EBITDA ratio. This suggests that LYLT has some financial stability and can potentially weather the storm.

Additionally, the analyst points out that the selling pressure on LYLT's stock has contributed to its current pricing, indicating that market sentiment may not accurately reflect the company's true value.

Therefore, with improvements in its operations and a shift in market perception, LYLT has promising future prospects.

Frequently Asked Questions

What Were the Factors That Contributed to Lylt's Decline Since Its Spin-Off From Alliance Data?

Since its spin-off from Alliance Data, several factors have contributed to LYLT's decline. These include the impact of the pandemic on its operating performance, the loss of Sobeys as a customer, and the challenges faced during the spin-off process.

How Has the Pandemic Affected Lylt's Operating Performance?

The pandemic has significantly affected Loyalty Ventures' operating performance. The loss of customers had a negative impact on the company, along with other factors such as goodwill impairment charges and a decline in free cash flow.

What Impact Did the Loss of Sobeys as a Customer Have on Lylt?

The loss of Sobeys as a customer had a significant negative impact on LYLT. It forced the company to reassess its strategies and find ways to replace the lost revenue.

What Are the Potential Risks and Challenges That LYLT Faces?

LYLT faces potential risks and challenges in its survival as a loyalty ventures company. These include customer attrition, recession, microcap volatility, perception concerns, cash flow doubts, potential insolvency risk, and the commoditization of rewards management.

What Is the Current Debt Situation of LYLT and How Could It Potentially Impact the Company's Future?

LYLT's current debt situation could potentially impact the company's future. The debt, which doesn't mature until 2026/2027, coupled with selling pressure, has contributed to current pricing. However, with time and improvement, LYLT could provide considerable gains.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.