MercadoLibre MELI and Alibaba BABA operate dominant e-commerce ecosystems in large emerging markets while also controlling sizeable digital payments platforms. MercadoLibre has established a leading position across Latin America through Mercado Libre and Mercado Pago, while Alibaba remains one of China’s largest online commerce and fintech ecosystems through Taobao, Tmall and its affiliated payment infrastructure.

Both companies reveal contrasting investment priorities, with MercadoLibre leaning into credit expansion and free shipping while Alibaba leans into cloud infrastructure and AI monetization. This divergence in execution offers a useful lens for evaluating which platform holds a more durable path to profitable growth. Let’s delve deep to determine which stock holds an edge.

The Case For MELI

MercadoLibre’s growth strategy continues to lean heavily on subsidies rather than structural efficiency. Revenue grew 49% year over year in the first quarter, yet operating margin compressed to 6.9%, indicating how closely growth and cost intensity remain linked. Lower free shipping thresholds in Brazil have lifted volumes, but the model depends on continued spending to sustain that demand, leaving little room for the cost base to improve on its own.

The fintech business adds further uncertainty. Mercado Pago’s credit portfolio nearly doubled to $14.6 billion, growing 87% year over year and far outpacing overall revenues, while the cost of risk has climbed toward 37% as the company extends loan durations and reaches into riskier borrower segments. This trajectory suggests provisioning pressure is likely to persist rather than ease, deepening exposure to credit cycles that can shift quickly across Latin America.

Competitive intensity is forcing MercadoLibre into defensive pricing actions, including lower seller take rates in Brazil set to flow through results from the second quarter of 2026 onward, adding fresh margin pressure on top of existing investments. Investment intensity appears set to stay elevated rather than ease, since margin levels are being shaped by the pace of reinvestment rather than by a defined profitability target, leaving the timeline for margin recovery open-ended.

The Zacks Consensus Estimate for 2026 earnings is pegged at $40.97 per share, up 3.98% year over year, with the modest pace of growth pointing to limited near-term margin recovery.

MercadoLibre, Inc. Price and Consensus

MercadoLibre, Inc. price-consensus-chart | MercadoLibre, Inc. Quote

The Case for BABA

Alibaba’s ecommerce business, built around Taobao and Tmall, functions as a maturing platform model where growth is shifting from raw transaction volume toward deeper merchant monetization. Customer management revenue returned to 8% growth on a like-for-like basis during the fourth quarter of fiscal 2026, suggesting the core marketplace can still extract more value per transaction, even as overall ecommerce growth across China moderates.

Quick commerce has become Alibaba’s main lever for extending its ecommerce footprint into adjacent categories such as groceries and daily essentials, a segment where unit economics are still being built out. Revenues from this segment rose 57% year over year to RMB20 billion, with order volumes reaching 2.7 times the prior year level and unit economics improving sequentially, while management is targeting profitability by the end of fiscal 2027.

However, international commerce continues to operate close to breakeven rather than profitably, with revenue growing 6% and losses narrowing as logistics efficiency improves. Collectively, the domestic marketplace, quick commerce and international operations give Alibaba several distinct ecommerce growth lines, though two of the three are still dependent on continued investment rather than self-funding their own expansion.

The Zacks Consensus Estimate for fiscal 2027 earnings is pegged at $7.38 per share, up 89.72% year over year, indicating the extent to which AI and cloud monetization are expected to offset near-term investment costs.

Alibaba Group Holding Limited Price and Consensus

Alibaba Group Holding Limited price-consensus-chart | Alibaba Group Holding Limited Quote

Price Performance and Valuation of MELI and BABA

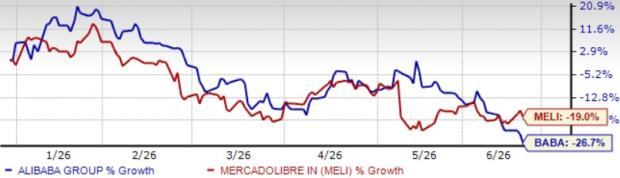

Year to date (YTD), both stocks have declined, with Alibaba’s plunge steeper at 26.7% against MercadoLibre’s 19%. The sharper pullback in BABA appears more tied to tariffs and broader China sentiment, even as Alibaba’s underlying business mix remains structurally stronger than MercadoLibre’s

YTD Performance

Image Source: Zacks Investment Research

On a forward 12-month price-to-sales basis, MercadoLibre trades at 1.83X against Alibaba’s 1.52X, leaving Alibaba at a relative discount despite its steeper YTD decline. The gap suggests MercadoLibre’s growth is being valued more richly even as its margin trajectory remains less certain, while Alibaba’s lower multiple points to a more diversified revenue base being priced at a relative discount.

Forward 12-Month (P/S) Valuation

Image Source: Zacks Investment Research

Conclusion

Both MELI and BABA continue to prioritize long-term positioning over near-term profitability, with MercadoLibre leaning on credit expansion and shipping subsidies while Alibaba leans on quick commerce expansion and deeper merchant monetization. Alibaba’s more diversified ecommerce growth lines and lower valuations make it the more durable pick, while MercadoLibre’s expanding and increasingly risky credit book leaves its margin recovery less certain.

BABA currently carries a Zacks Rank #3 (Hold) against MELI’s Zacks Rank #5 (Strong Sell), suggesting that existing investors may continue to hold BABA while staying away from MELI.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA’s enormous potential back in 2016. Now, he has keyed in on what could be “the next big thing” in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

MercadoLibre, Inc. (MELI) : Free Stock Analysis Report

Alibaba Group Holding Limited (BABA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.