Ford F is heading into the back half of 2026 with one less risk on the table. It has announced a tentative three-year agreement with Unifor covering more than 5,000 Canadian workers, with talks centered on better pay, benefits and job protections. The deal still needs member ratification, but landing it well ahead of the Sept. 20 contract expiration matters. That takes strike risk off the table at a time when the auto industry is already grappling with the electric vehicle (EV) transition and shifting demand.

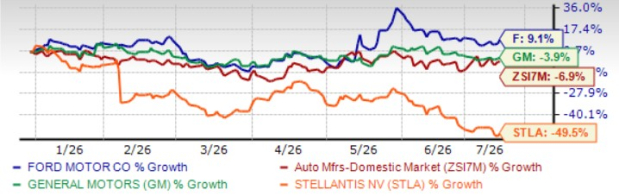

Ford is up 9% year to date, outpacing the industry’s loss over the same period. The stock has also outperformed its closest peers, General Motors GM and Stellantis STLA, which witnessed their shares decline over the same timeframe.

YTD Price Performance Comparison

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

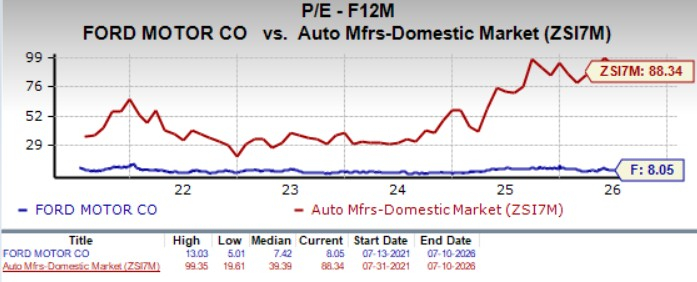

The stock is trading at 8.05X forward earnings (at a huge discount relative to the industry), with a Value Score of A. Yes, there are a few challenges in Ford’s path, including losses in its EV business, ongoing recalls and tariff costs, but there are various factors working in favor of the stock.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Ford’s 2026 and 2027 EPS implies year-over-year growth of 50% and 12%, respectively. The consensus mark for 2026 and 2027 EPS has moved up over the past 60 days.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Here are four key reasons why we are bullish on Ford stock.

Ford Pro Is the Key Growth Engine

Ford’s commercial vehicle and services unit, Ford Pro, is turning into the company’s most important segment. Even with wholesale volumes down 10% in the last reported quarter due to supply issues, the unit still grew EBIT by $376 million year over year and held an 11.4% margin — a sign the business is getting structurally stronger, not weaker. Software subscriptions jumped 30% year over year to 879,000 in the first quarter, and the ServiceTitan partnership is deepening Ford’s digital lock-in with commercial customers. Management expects $6.5-$7.5 billion in EBIT from Ford Pro this year.

Ford Energy Adds a New Growth Leg

Ford is building an energy storage business beyond vehicles. The company plans to invest $1.5 billion in 2026 toward 20 GWh of battery storage capacity by 2027, split across its Kentucky and Michigan facilities. This isn’t just an EV side-project — it’s a real attempt to diversify revenues using Ford’s existing manufacturing scale. The unit landed its first major customer in May, a five-year battery storage supply deal with EDF Power Solutions North America.

Ford’s Novelis Supply Problem Is Resolving

A major drag on Ford’s results has been the aluminum shortage caused by fires at supplier Novelis’s Oswego, NY, plant, which supplies material for F-Series trucks. That disruption cost Ford roughly 100,000 trucks in 2025 and around $2 billion in losses. The good news is that Novelis restarted operations at Oswego last month, and Ford is targeting recovery of about half the lost truck volume as production ramps in the second half of 2026. Both Ford Pro and Ford Blue should benefit as truck output normalizes.

Ford’s Balance Sheet Strength

Ford closed the first quarter of 2026 with $22 billion in cash and $43.1 billion in total liquidity— a strong cushion while it funds EV development, energy storage and software simultaneously. That gives management room to execute even if the macro backdrop worsens. On top of that, Ford’s dividend yield sits above 4%, more than triple the S&P 500 average, boding well for income investors.

Last Word

Ford’s story is shifting from a legacy automaker weighed down by EV losses to a diversified industrial platform with real margin drivers. Labor stability, a recovering supply chain, and two emerging high-margin businesses in Ford Pro and Ford Energy give the stock multiple paths to upside that the market hasn’t fully priced in. Trading at a steep discount to the industry while paying a 4%+ dividend, Ford offers a rare combination of value, growth and income. We recommend buying Ford stock at current levels.

The stock sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks’ Research Chief Names “Stock Most Likely to Double”

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company’s customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners Up

Ford Motor Company (F) : Free Stock Analysis Report

General Motors Company (GM) : Free Stock Analysis Report

Stellantis N.V. (STLA) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.