In a shortened and fairly quiet week in regards to the earnings lineup, a few top-rated Zacks stocks are standing out before their quarterly results.

As investors await earnings from Microsoft MSFT and Netflix NFLX next week, 1ST Source SRCE and Fastenal FAST are two companies that shouldn’t be overlooked ahead of their fourth quarter reports on Thursday, January 18.

Fastenal Q4 Preview & Overview

Fastenal is one of the most appealing retailers at the moment as a national wholesale distributor of industrial and construction supplies. Infrastructure and construction-related activities including homebuilding have continued to thrive with Fastenal’s stock up +32% over the last year to easily top the Zacks Building Products-Retail Markets’ +10% and the S&P 500’s +20%.

Image Source: Zacks Investment Research

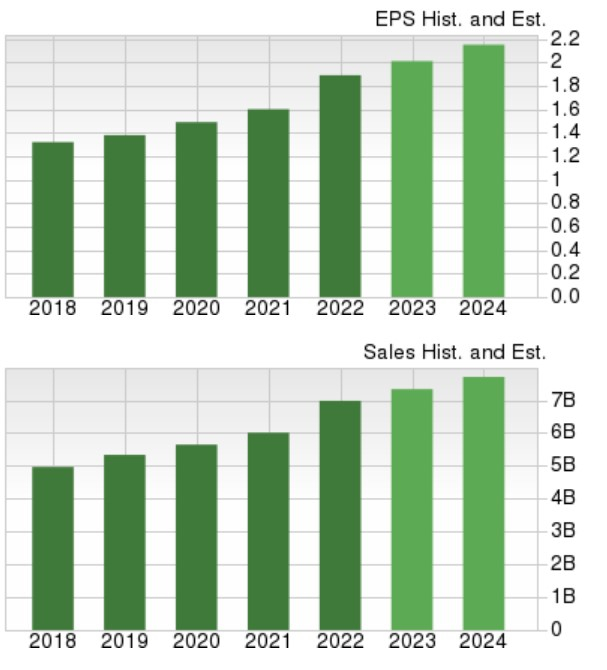

For the fourth quarter, Fastenal’s earnings are expected to be up 4% year over year to $0.45 a share with sales projected to rise 3% to $1.75 billion. Overall, Fastenal is expected to round out fiscal 2023 with annual earnings up 6% to $2.00 a share and total sales up 5% to $7.34 billion. Even better, Fastenal is projected to have another 6% growth on its top and bottom lines in FY24. Fastenal also offers investors a generous 2.20% annual dividend yield.

Image Source: Zacks Investment Research

1ST Source Q4 Preview & Overview

Ahead of its Q4 results, 1ST Source is a regional bank enjoying positive earnings estimate revisions with general banking branches throughout Indiana and Michigan.1ST Source’s stock is down -5% in the last year but looks attractive at a 12.3X forward earnings multiple which is near the Zacks Banks-Midwest Industry average of 10.6X and well below the S&P 500’s 20X. 1ST Source’s 2.63% annual dividend yield also bolsters its more attrctive valuation.

Image Source: Zacks Investment Research

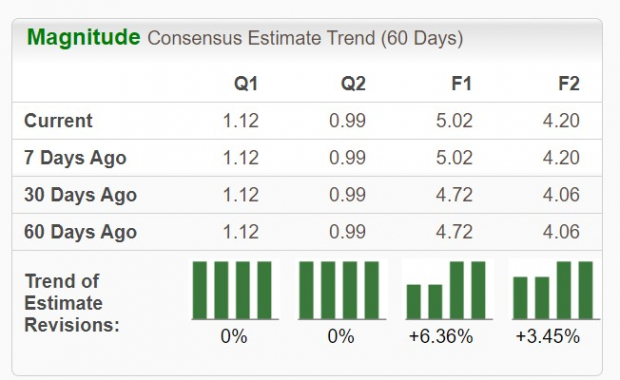

1ST Source’s stock appears to have already priced in Q4 earnings being forecasted to dip -10% YoY to $1.12 a share with sales expected to be down -4% to $91.2 million. Also rounding out its FY23, annual earnings are still projected to rise 4% to $5.02 per share but are expected to dip to $4.20 a share in FY24. However, over the last 60 days, FY24 earnings estimates are up 3% while FY23 EPS estimates have risen 6%. Total sales are now slated to rise 4% in FY23 and then dip -3% this year to $356.7 million but 1ST Source’s price-to-sales ratio of 2.6X is closing in on the optimum level of less than 2X.

Image Source: Zacks Investment Research

Takeaway

Fastenal and 1ST Source look like two stocks that could rally if they post favorable Q4 results and guidance. At the moment, 1ST Source’s stock covets a Zacks Rank #1 (Strong Buy) in correlation with its attractive valuation and rising earnings estimates while Fastenal’s stock sports a Zacks Rank #2 (Buy) and remains a very intriguing option for growth.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.