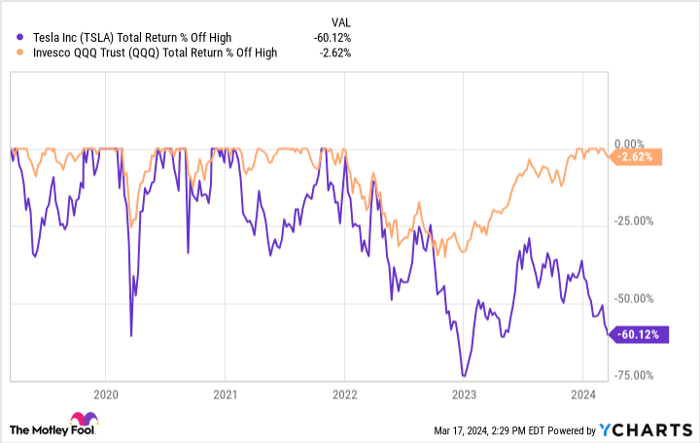

The stock market is on the rise once again, but the iconic electric vehicle (EV) powerhouse, Tesla (NASDAQ: TSLA), is not taking the lead. Despite the market upsurge, Tesla shares have plummeted by a staggering 34% year to date, while the Nasdaq-100 index continues its upward trajectory. Currently, Tesla’s stock stands 60% below its all-time peak even as the broader market approaches new highs.

At this juncture, the future of Tesla stock hangs in the balance, with advocates making a case for a prime buying opportunity in anticipation of the company’s next growth phase. Conversely, detractors argue that Tesla is simply gravitating towards a more conventional valuation befitting a manufacturing-centric enterprise.

Unit Growth vs. Margins Squeeze

In 2023, Tesla sustained its expansion in unit volumes, delivering a remarkable 1.8 million cars worldwide, surpassing the figures of 1.3 million in 2022 and 936,000 in 2021. This notable surge in scale positions Tesla as a leading manufacturer, not only in the EV realm but across the automotive landscape. For comparison, the world’s largest automaker, Toyota, produces just over 10 million vehicles annually.

However, this growth in units has come at a cost – Tesla has had to reduce its prices. The company’s focus has shifted towards more affordable models like the Model 3 and Y, steering away from its pricier X and S models. Concurrently, Tesla has been compelled to slash prices on the Model 3 and Y to drive volumes, a move reflected in the steep drop in the resale value of used Teslas, which has halved since early 2022.

Consequently, the decline in prices has led to a deceleration in revenue growth and a squeeze on margins. Despite a 19% revenue increase to $97 billion in 2023, growth tapered to a mere 3% in the fourth quarter. Gross margins contracted from 25.6% in 2022 to 18.2% in 2023, resulting in a 35% decline in operating income for the year. The pursuit of global scale is gradually eroding Tesla’s profit margins.

Innovation: The Key to Future Growth?

To further widen its consumer base, Tesla may need to introduce an even more cost-effective vehicle. The ability to sell only a limited number of vehicles priced at $40,000 or above underscores the necessity for Tesla to unveil a more budget-friendly model. Speculation suggests the launch of such a vehicle around 2025, as hinted by CEO Elon Musk in a recent earnings call. However, given Musk’s flexible timelines, the arrival of a new product by 2025 remains uncertain, though a new offering in the near future seems plausible.

While a new vehicle launch could bolster Tesla’s volumes, a lower price point of approximately $25,000 may lead to revenue growth lagging behind unit volume expansion, as the average selling price of Teslas continues to decline. Investors must consider this dynamic while forecasting Tesla’s revenue prospects in the forthcoming years.

Valuation and Future Earnings

Forecasting Tesla’s stock trajectory in three years requires an estimation of its financial path. Assuming a tripling of volumes compared to 2023 due to the successful rollout of a more affordable vehicle, revenue could potentially double owing to reduced average selling prices. Maintaining profit margins similar to 2023 at 9.2%, Tesla could achieve earnings of $17.8 billion in three years.

Presently, Tesla commands a market cap of $512 billion. With estimated future earnings of $17.8 billion, the price-to-earnings ratio stands at 29, slightly surpassing the market average. This suggests that Tesla’s stock may remain stagnant in the upcoming years, indicating a lack of undervaluation even after the recent pullback, posing a potential value trap for investors.

Those considering buying the dip must exhibit heightened optimism regarding the company’s future growth prospects. Otherwise, Tesla’s stock could remain stagnant for an extended period.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.