Apparel behemoths like Lululemon (LULU) and Nike (NKE) have not escaped the shadow of apprehension surrounding a potential slowdown in consumer spending, with both stocks plummeting roughly 8% over the past year. Nevertheless, Lululemon has demonstrated resilience by surpassing Q1 earnings expectations, underscoring its promising growth trajectory. Nike is poised to unveil its quarterly results later this month.

In the wake of LULU’s 37% year-to-date decline, investors are pondering the potential for acquiring shares in this iconic yoga-inspired athletic wear company, given its illustrious historical performance.

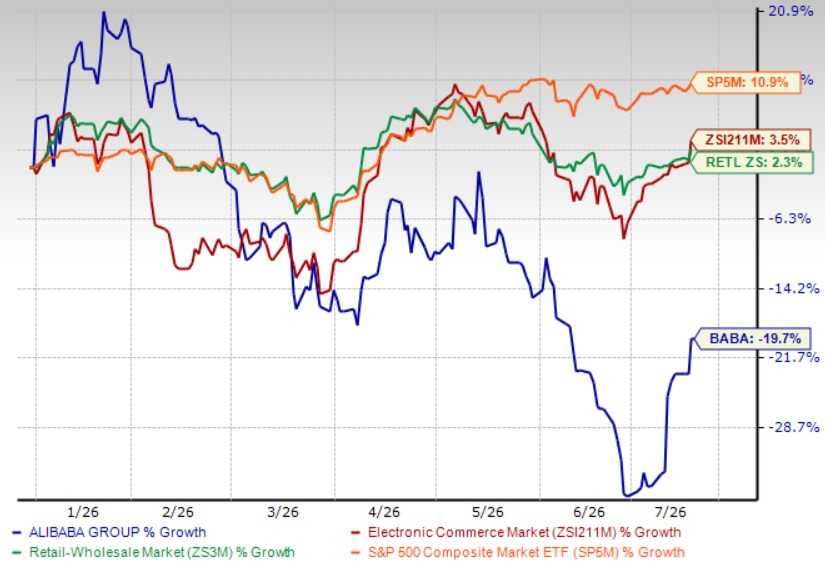

Image Source: Zacks Investment Research

Q1 Performance & Future Outlook

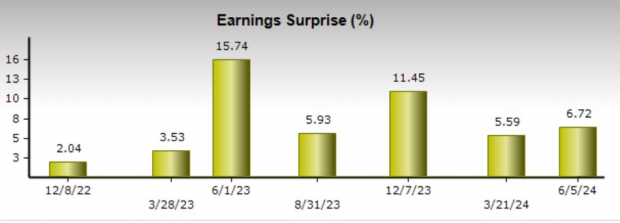

Underlining its robust brand loyalty, Lululemon posted Q1 sales of $2.2 billion, marking a 10% increase from the preceding quarter and marginally exceeding estimates of $2.19 billion. Furthermore, Q1 EPS of $2.54 outperformed expectations by 7% and surged 11% from the previous year. It is worth noting that Lululemon has now outperformed earnings projections for 16 consecutive quarters since September 2020.

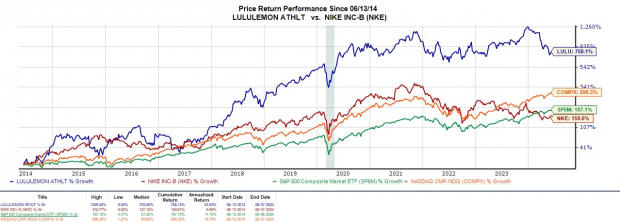

Image Source: Zacks Investment Research

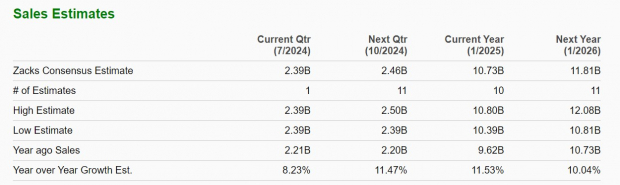

For the upcoming quarter, Lululemon anticipates a revenue increase between 9% to 10%, slightly surpassing the current Zacks Consensus projection of 8.23% growth or sales of $2.39 billion. The company’s full-year revenue outlook remains favorable, with expected growth in the range of 10% to 11% and a forecasted growth rate of 11.53% for the current fiscal year.

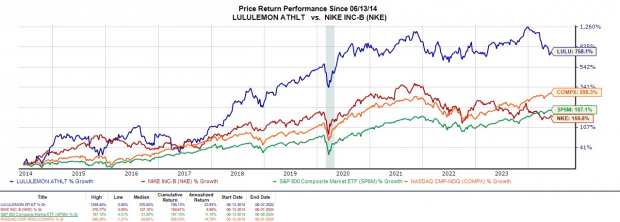

Image Source: Zacks Investment Research

Earnings Projection

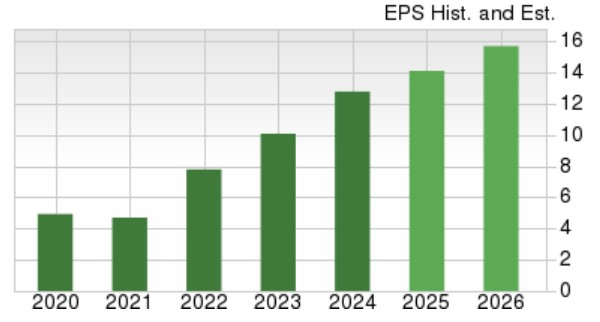

According to Zacks estimates, Lululemon’s annual earnings are projected to climb by 11% in the current fiscal year 2025, reaching $14.14 per share compared to $12.77 in FY24. Furthermore, FY26 EPS is expected to leap by another 11% to $15.68.

Image Source: Zacks Investment Research

Key Takeaways

Despite prevailing concerns regarding a deceleration in consumer spending, particularly on high-end apparel items, Lululemon’s stock maintains a Zacks Rank #3 (Hold). The Q1 results further reinforce the optimistic earnings outlook for the company. Additionally, LULU is trading at one of its most attractive price-to-earnings valuations since its IPO at 22.9X, indicating that long-term investors could reap rewards from the current levels, while potentially better buying opportunities could lie ahead.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.