Despite its long history as a stalwart of American auto manufacturing, Ford currently finds itself languishing in the bargain bin, its stock trading at a significant discount. Viewed through the lens of valuation, the numbers tell quite the tale. With a forward sales multiple of 0.26, Ford is residing below its own five-year average, creating an aura of allure for value-hungry investors. In comparison to its industry counterparts, such as the venerable General Motors, Ford’s valuation appears especially compelling. Awarded a Value Score of A, Ford’s allure is not without merit.

Ford’s Undervalued Shares

Further bolstering Ford’s appeal are its cash flow metrics, demonstrating a robust financial position. Notably, Ford lifted its adjusted Free Cash Flow (FCF) projection for 2024 by an additional $1 billion during its recent earnings call, now anticipating a range of $7.5-$8.5 billion. The company’s price-to-cash flow ratio further solidifies its prevailing value proposition, presenting investors with an opportunity to acquire a fundamentally strong asset at a discounted rate.

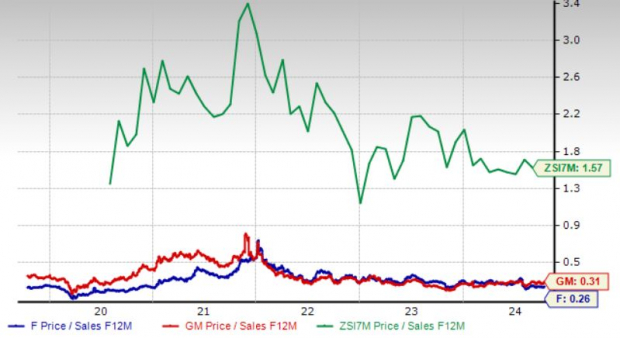

The famed Price-to-Cash Flow (P/CF) ratio, cherished by seasoned investors for its reliability in discerning a company’s fiscal soundness, stands at a tantalizing 3.09 for Ford. This figure starkly contrasts the industry’s historical average of 19.19, positioning Ford as a captivating option for value-minded traders.

Burdened by a sluggish stock price, Ford beckons intrepid shareholders to explore its growth prospects and hurdles in determining whether an investment in the company warrants pursuit at this juncture.

Fortifying Ford Pro Unit to Drive Performance

Ford’s commercial vehicle and services division, Ford Pro, emerged as a beacon of success during the second fiscal quarter. Witnessing EBIT escalation by 7% to $2.6 billion, coupled with a 15% margin, the segment’s commendable performance enabled revenue growth to soar by 9% to $17 billion. Noteworthy was the elevated demand for Super Duty trucks and Transit vans, prompting Ford to announce a forthcoming assembly plant in Ontario by 2026, designed to accommodate 100,000 Super Duty units.

The operational prowess of Ford Pro, celebrated for its robust order pipeline and escalating demand signals, coupled with the triumphant debut of the all-new Super Duty, lays a strong foundation for the segment’s anticipated success. By upping the EBIT forecast for Ford-Pro from $8-$9 billion to $9-$10 billion, Ford underscores the unit’s strategic importance, buoyed by sustained growth in vehicles, software, and physical services.

Robust Liquidity and Rewarding Returns Foster Confidence

Closing the second quarter of 2024 with $27 billion in cash and a liquidity cache exceeding $45 billion, Ford fortifies its financial backbone to fuel investments in its Ford+ initiatives. The company’s munificent dividend yield of over 5% starkly outshines the S&P 500’s modest 1.23% average yield, underlining Ford’s commitment to delivering value to its loyal shareholder base. Maintaining a target of distributing 40-50% of FCF moving forward underscores Ford’s unwavering dedication to returning value to its investors.

Ford’s Dividend Yield (TTM)

Assessing Ford’s Electric Vehicle Ventures

Amid a burgeoning EV marketplace, Ford’s foray into electric vehicles is gaining traction, buoyed by popular offerings like the Mustang Mach-E, E-Transit vans, and F-150 e-pickup. With Ford brand EV sales surging by 45% in the initial nine months of 2024, the company positions itself as a formidable contender in the U.S. EV market, trailing solely behind Tesla.

Moreover, sales of the electric F-150 Lightning doubled in the third quarter, while the E-Transit recorded a 13% uptick with 2,955 units sold. Ford’s roadmap includes introducing a commercial electric van in 2026 and two new pickup trucks in 2027, alongside commencing battery cell production at its Tennessee facility in 2025, a strategic move to fortify its EV supply chain.

Despite these positive strides, Ford’s immediate EV outlook appears challenged. Having incurred losses of $4.7 billion in its EV segment, Ford anticipates an intensification of losses to $5-$5.5 billion in the current year, accentuated by pricing pressures and amplified investments in forthcoming EV models.

Perils Amid Potential: The Case Against Investing in Ford

Beyond the struggles in the EV arena, Ford grapples with a revised 2024 EBIT forecast for its Blue unit, focusing on traditional Internal Combustion Engine (ICE) and hybrid models. Trimming the unit’s projected earnings to $6-$6.5 billion (down from approximately $7.5 billion in 2023) due to soaring warranty costs, Ford encountered compounded challenges with warranty and recall expenses escalating to $2.3 billion in the second quarter of 2024.

While Ford strives to enhance the quality of its newer models, mitigating warranty expenses may entail a prolonged timeline of 12 to 18 months. This trajectory suggests that Ford’s financial burden from warranty claims may endure, curbing profitability in the interim.

Estimates for Ford’s 2024 EPS hint at a year-over-year contraction of 6.5%, with projections for 2024 and 2025 EPS receding by 2 cents and 4 cents, respectively, over the preceding 60 days.

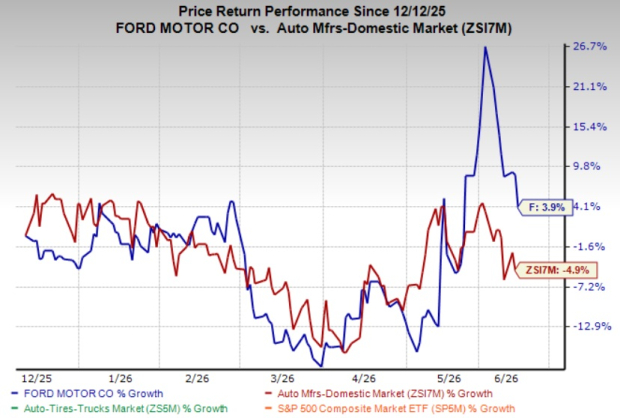

While Ford’s diminished valuation, mirrored in a 12% decline over the past half-year, hints at an opportune entry point for investors, the company’s imminent impediments suggest caution. Those with a proclivity for long-term investing may find merit in retaining their current holdings rather than initiating fresh positions at this juncture.

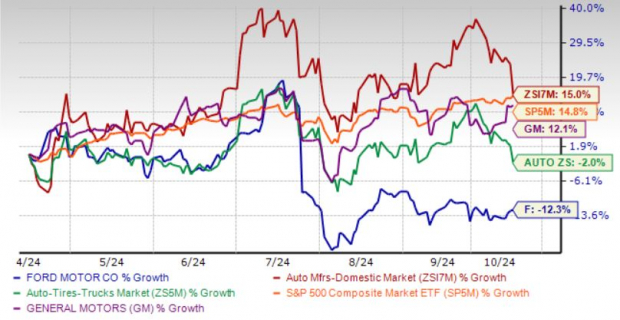

Ford’s Recent Stock Performance

Ford presently holds a Zacks Rank #3 (Hold), reflecting a stance of restrained optimism. For those seeking opportunities in the equity market, exploring the complete list of today’s Zacks #1 Rank (Strong Buy) stocks may unveil hidden gems.

Discover the Top 7 Stock Picks for the Next 30 Days

Investing enthusiasts can now explore a curated list of 7 standout stocks identified by experts amongst the existing roster of 220 Zacks Rank #1 Strong Buy selections. These securities are earmarked for early price upsurges, with a historical track record dating back to 1988, outperforming the market twofold with an average annual gain of +23.7%. Seize the moment and pay special attention to these elite 7 stock picks.

Stay informed with the latest recommendations from Zacks Investment Research by obtaining a complimentary report on 5 Stocks Poised to Double. Embrace the journey of informed investing.

Embark on your investment quest here.

Acquire strategic insights into Ford Motor Company (F) by perusing a detailed Stock Analysis Report here.

Explore comprehensive analytics on General Motors Company (GM) through a detailed Stock Analysis Report here.

Delve into the financial intricacies of Tesla, Inc. (TSLA) by accessing a comprehensive Stock Analysis Report here.

For further exploration on Ford’s current status, engage with the complete article on Zacks.com here.

For more financial insights and market trends, visit Zacks Investment Research here.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.