Alibaba’s Resurgence in Growth Signals a Bright FY2025

Alibaba, a stalwart in the world of e-commerce, reported promising results in its Q4-2024, ending March 31st. With revenues reaching $30.7 billion, up by 7% year-over-year, the company’s full-year revenues hit $130.4 billion, an 8% increase from FY2023. Notably, this rebound in growth stands out from the prior year, where revenue growth had stagnated at just 2%, nearly flatlining.

The growth wasn’t confined to one area for Alibaba, with its core e-commerce platforms experiencing a steady increase in revenue, driven by a surge in buyers and purchase frequency. Both Taobao and Tmall saw a 4% year-over-year revenue growth. The momentum extended internationally, with Alibaba International Digital Commerce (AIDC) witnessing an outstanding 45% revenue increase, fueled by solid combined order growth and monetization enhancements.

Alibaba’s Cloud Intelligence segment saw a more modest 3% revenue growth compared to the previous year. However, advancements in core public cloud offerings and AI-related revenues suggest a potential acceleration in growth for this segment in the near future. The company’s strategic positioning in the AI sector within China also presents a unique competitive advantage, given its substantial scale in cloud computing.

Driving Profitability, Valuation, and Capital Returns

Alibaba’s return to growth in FY2024 translated into impressive profitability enhancements, propelled by the company’s remarkable economies of scale. Notably, Alibaba recorded a 12% growth in adjusted EBITA to $22.9 billion, with the adjusted EBITA margin expanding from 17% to 18%. The company’s adjusted net income also rose by 11% to $21.8 billion, with a per-ADS figure climbing by an even more substantial 14% to $8.62, aided by share buybacks.

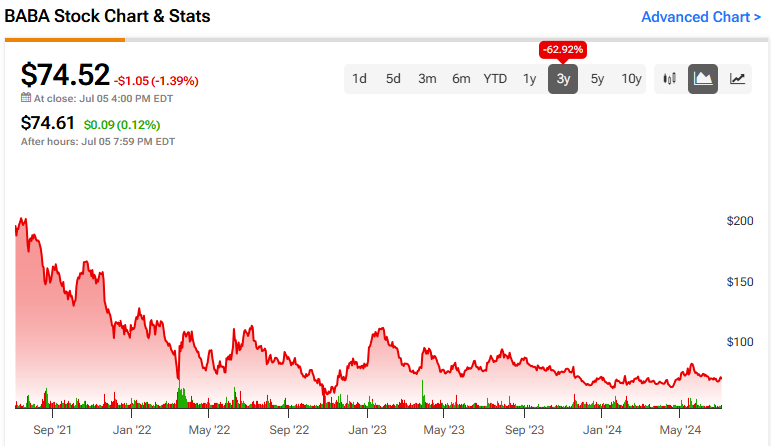

Despite Wall Street’s projected moderation in Alibaba’s ADS this year, with a consensus estimate of $8.20 for FY2025, signaling a slight decline of 4.7%, the stock continues to trade at an exceptionally low forward P/E ratio of 9x. Alibaba’s focus on capital returns through share repurchases and dividends, with dividends totaling $1.66 per ADS this year, adds to the stock’s attractiveness. The stock already boasts a high single-digit total yield, making it a compelling proposition for investors.

Analysts’ Take: Is BABA Stock a Buy?

Wall Street analysts maintain a bullish stance on Alibaba, given its undervalued state. With a Strong Buy consensus rating backed by 14 Buy recommendations and three Holds, the average BABA stock price target of $103.70 indicates a substantial upside potential of 39.2%, showcasing significant room for growth.

The Final Word

Alibaba’s stock, despite past underperformance, is showing promising signs of a turnaround. With growth reverberating through FY2024 and positive indicators for the upcoming fiscal year, Alibaba’s investment proposition appears increasingly compelling. Coupled with the recent emphasis on capital returns, including substantial share buybacks and a growing dividend, Alibaba seems poised to regain investor confidence and reignite bullish sentiment.

As with any investment, risks remain inherent, especially with a company of Alibaba’s stature. However, at its current valuation, the potential rewards seem to overshadow these risks. Alibaba’s blend of growth potential and capital returns presents a tantalizing opportunity for investors looking to capitalize on the e-commerce giant’s resurgence.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.