Alibaba has trudged through a desert of lackluster stock performance, weathering regulatory storms and global economic pressures. In its recent financial unveiling, the giant revealed feeble revenue growth and dwindling income, deepening the shadows of skepticism shrouding its shares. Despite this gloom, Alibaba’s vigorous stock repurchases emerge as a beacon of hope amidst the prevailing gray clouds, especially as the shares continue to dawdle at a somber valuation. This gesture hints at a potential shift on the horizon – a reason for optimism in the midst of adversity.

Alibaba’s Sluggish Revenue and Earnings

The recent fiscal quarter of 2025 wasn’t Alibaba’s finest hour, showcasing a stumbling trajectory as its revenue growth lost steam amidst the e-commerce and cloud domain. Yet, beyond the conventional narrative lie elements that buoy my optimism, reasons I shall soon explore. Initially, let’s delve into Alibaba’s financial realm.

In Q1, the total revenue floundered at $33.47 billion, marking a meager 3.9% ascent from the prior year. This sluggish pace starkly contrasts with last year’s 13.9% leap and the preceding quarter’s more modest 6.6% climb.

Within this chapter, Alibaba’s vitality stemmed from the international commerce sphere and cloud domain, while its domestic trade hub – Taobao and Tmall – saw a diminutive revenue descent. Particularly, China’s commerce retail section saw a 2% sales drop to approximately $14.8 billion.

Constrictions in direct sales initiatives imposed a weighty toll on these metrics. Although customer management revenue edged up by 1%, it was outmatched by a dip in the company’s take rate – the cut Alibaba earns from its platform transactions.

Despite strides in operational efficiency, Alibaba’s adjusted net income tumbled by 9% to $5.6 billion. While the company sought to augment core e-commerce platforms and expand globally, its operating margin slid from 18% to 15%, singed by augmented investments in cloud and logistics sectors operating at slimmer margins – essential for Alibaba’s future yet reigning as present drags.

Surging Buybacks: A Potential Bullish Catalyst

Although Alibaba’s financial doses left a sour palate, providing sinew to the looming negativity, the persistent cadence of stock buybacks could potentially realign the narrative towards optimism. This bedrock upholds my favorable stance on the narrative spun around the Alibaba stock.

Zeroing in, the quarter witnessed Alibaba snapping up 613 million shares at $5.8 billion, rounding up the annual buyback spree to a stately $18.1 billion. This showcases a repurchase yield of 9.4% at the prevailing market cap. Such assertive buyback undertakings underscore management’s faith in Alibaba’s intrinsic worth, even as its market value slumbers.

Moreover, in a landscape where Chinese enterprises seldom engage in such buybacks, Alibaba’s resolute repurchasing strategy stands as a sentinel of management’s conviction that current valuation levels hold promise for future per-share metrics. While Alibaba’s latest figures might lack sheen, it remains a cash-heaving barge in comparative realms.

Peeling another layer, Alibaba is projected to rake in a free cash flow of $21.7 billion in Fiscal 2025. The following year anticipates a leap to $25.2 billion, with capital expenditures poised to taper. These numbers translate to a current and forthcoming P/FCF ratios of 8.9 and 7.6, correspondingly – illuminating subdued valuations, even for a fleet-footed tortoise.

Hence, with this considerable pool of free cash flow salting buybacks at enticing price points, nearly touching double digits yields, Alibaba’s investment narrative caverns a sturdy sanctuary with substantial upside potential at its current mooring.

Another intriguing facet is Alibaba’s burgeoning dividend disbursements, dovetailing with the prevailing buyback yield to conjure a double-digit shareholder deluge at current echelons.

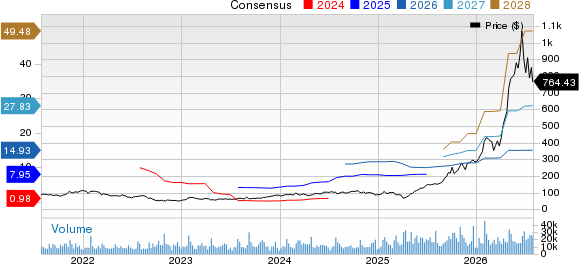

Is BABA Stock a Buy, According to Analysts?

A cursory glance at Wall Street’s tableau on BABA stock exposes a Strong Buy consensus, rooted in 13 Buy endorsements folded with three Holds over the past quarter. With the average Alibaba stock forecast perched at $109.53, a 34.92% elevating vista unfurls.

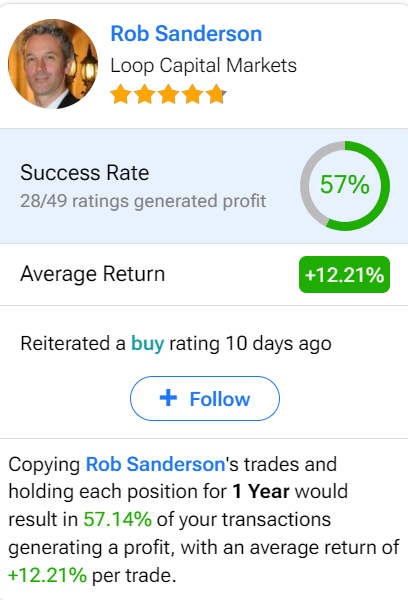

Floating amidst the cacophony of analyst voices advocating on Alibaba, a five-star oracle emerges in Rob Sanderson from Loop Capital Markets. Over the past year, he has danced to the most melodious tunes, yielding an average return of 12.21% per proclamation, sporting a feather-capped 57% success rate. The sage beckons, offering a path through the clutter.

Takeaway

In the coda of this bullish hymn, Alibaba’s acrobatics with revenue growth and a receding income haven’t exorcised my optimism, not with the company’s bold foray into share buybacks. With a robust free cash flow and a muted valuation, Alibaba’s stock poses a tantalizing tableau at current vantage points. The ongoing buybacks are poised to cradle the share value, knitting per-share metrics into a coat of safety margins and fostering a garden where earnings per share sprout and grow.

This tale of cautious yet anchored optimism endures, amidst Alibaba’s lengthy tryst with underperformance.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.