It’s a busy news cycle. Let’s bounce around to a handful of stories likely impacting your portfolio.

Inflation Remains a Thorn in The Federal Reserve’s Side

Earlier this week, the CPI number came in above forecasts causing a significant downturn on Wall Street. The fear that the hot CPI data would prompt the Federal Reserve to delay its initial rate cut while potentially cutting rates fewer times in 2024 led to substantial selling pressure. The hope was that the Producer Price Index (PPI) print would be more encouraging, giving the Federal Reserve members the “cool” data that they’re looking for. Instead, the number also came in higher than expected. The subsequent Wall Street response mirrors the reaction to Tuesday’s hot CPI report – poorly. The market understands that the Federal Reserve’s rate-cut decisions are based on inflation data. With today’s inflation data proving stubborn, the idea of numerous rate cuts in 2024 is dwindling. The futures market, which initially priced in the first rate cut in March, now shows ambiguity about a cut happening in June. If the inflation data continue to prove stubborn, next fall is the safer bet.

Red Sea Conflict Impacts Shipping Costs and Inflation

For several months, Houthi rebels have been attacking ships in the Red Sea, disrupting one of the world’s busiest trade routes. The Red Sea is the only route to the Suez Canal, making it a crucial trade route connecting Europe and the East. About 12% of global trade passes through the canal, representing 30% of all global container traffic. The longer transits resulting from these attacks are affecting shipping costs. While there is currently limited impact on consumer prices, if the situation doesn’t improve, it could change the inflation landscape. As global goods disinflation has been the primary driver of lower inflation around the world, even a modest rebound in goods inflation could render global core CPI inflation sticky around the 3% mark, which is 50% higher than the Fed’s target inflation rate.

Louis Navellier’s Bullish Outlook on Oil

Oil continues to climb, and investor Louis Navellier is feeling bullish about his Big Energy Bet. Energy stocks appear attractive for a trade both on a shorter-term basis and a longer-term basis. By utilizing his “Portfolio Grader” tool, Navellier provides a quant-investment perspective, evaluating the earnings strength of a stock based on key fundamental factors like sales growth and cash flow. His making of an “energy bet” signifies a broader market optimism amid the prevailing inflation concerns and Red Sea disruptions.

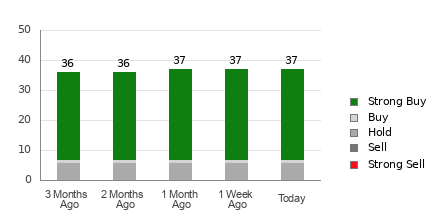

The Impact of Consumer Spending on the Economy

Phillips 66 is the only one with an active “buy” status today.

To take the Portfolio Grader for a test drive, just click here.

Lingering Effects of Retail Sales

Consumer spending fell hard in January, which indicates underlying weaknesses in the U.S. consumer market. According to CNBC, advance retail sales dipped by 0.8% in January, following a revised 0.4% upturn in December. Economists were expecting a drop of 0.3%, but in reality, sales plunged more than anticipated, particularly when excluding auto sales which declined by 0.6%.

It is clear that consumers overspent during the holidays, as the only areas that experienced an increase in spending were furniture sales and purchases at bars and restaurants.

However, in the current market environment, the decline in consumer spending provides the Federal Reserve with supporting data for a potential rate cut, which would aim to stimulate economic growth.

The bleak retail sales report is expected to prompt a downward revision of GDP forecasts, potentially leading to an earlier-than-expected rate cut by the Fed.

Warning Signs from Consumer Debt

Another cause for concern is the latest data on consumer debt. Credit card balances have surged by 10% compared to the previous year, reaching an all-time high average of $6,360.

While some of the elevated balances are due to inflation, the more concerning trend is the increasing number of Americans unable to pay off their credit card balances each month. Delinquency rates on credit card payments have jumped across the board, with serious delinquencies (those 90 days or more past due) reaching the highest level since 2009. This indicates that consumers are struggling with their debt payments, a trend that is expected to persist and intensify.

Both the decline in retail sales and the rising consumer debt may accelerate the timing of a Federal Reserve interest rate cut. The continuation of these trends could put considerable pressure on squeezed household budgets. The question remains whether the U.S. consumer will be able to endure until a potential interest rate cut by the Fed, or if sticky inflation data will delay the rate cut, causing consumers to curtail their spending later in the year.

Given the current inflation data, it appears that the situation is finely balanced. Further updates on these trends will be provided in the Digest.

Have a good evening,

Jeff Remsburg