Costco Wholesale: The Resilient Retailer

With the artificial intelligence (AI) revolution unfolding, giants like Nvidia and Amazon grab the spotlight. Still, amidst these tech titans lie diamonds in the rough – growth stocks with the potential to reward patient investors.

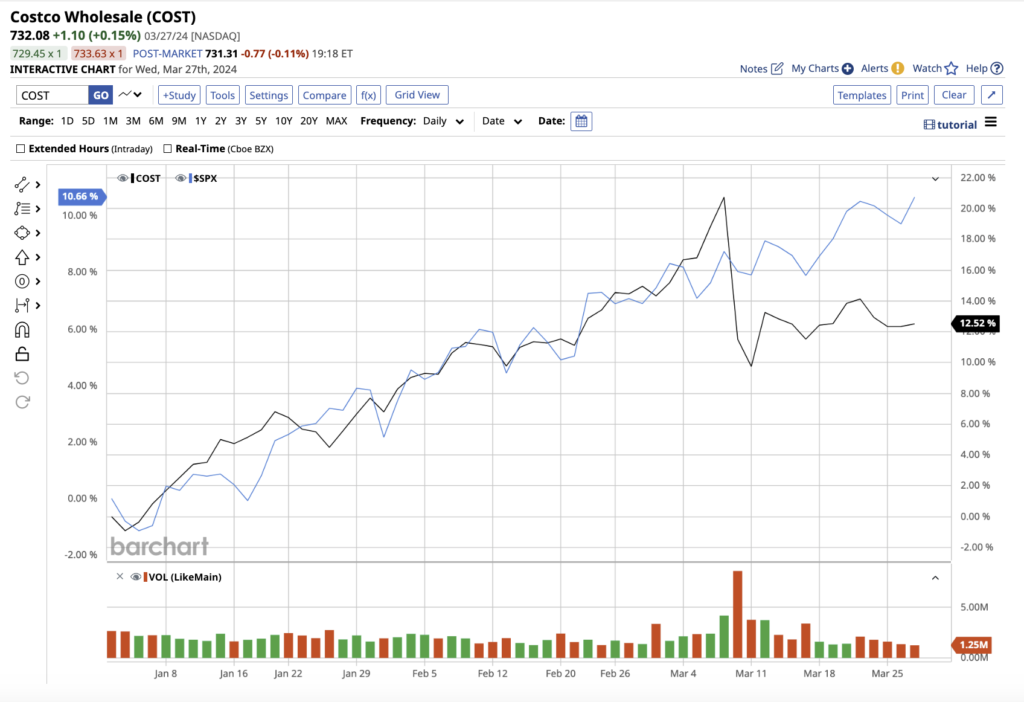

One such gem? Costco Wholesale (COST). While not as flashy as some hypergrowth stocks, Costco boasts remarkable resilience, with its shares soaring 556% in the last decade, leaving the S&P 500 in its dust.

Year-to-date, COST stock has surged by 11%, a testament to its enduring appeal.

One of Costco’s secrets to success lies in its lucrative membership-based model, offering exclusive deals to loyal customers while reaping the benefits of recurring revenue. In the second quarter of fiscal 2024, membership fees alone totaled $1.1 billion, up by 8.8% from the previous year.

The company’s global footprint, spanning 875 warehouses across multiple countries, shields it from market-specific risks while diversifying its income sources.

Moreover, Costco’s dividend yield and sustainable payout ratio underscore its financial health. Analysts foresee a 4.9% revenue upswing and a 12.4% earnings surge in fiscal 2024, with further growth projected in fiscal 2025.

Although COST stock may seem pricey compared to peers like Walmart, its resilience and innovation make it a standout choice for investors seeking long-term stability or a piece of the evolving retail landscape.

The Analyst Verdict on COST Stock

Wall Street sings a chorus of praise for COST, deeming it a “strong buy.” Among the 19 analysts covering the stock, all voice a resounding “strong buy” sentiment, underscoring confidence in its future.

The mean price target of $774.58 suggests a 5.7% upside potential, while the high target of $905 tantalizes with a lofty 23.5% gain in the next 12 months.

Marvell Technology: Riding the Semiconductor Surge

Amidst the AI wave, Marvell Technology (MRVL) shines brightly in the semiconductor industry. With demand for its AI products on the rise, Marvell’s impact spans high-performance networking solutions to cutting-edge storage technologies, fueling advancements in data centers, cloud computing, and 5G connectivity.

Valued at $62 billion, Marvell boasts a 17.5% year-to-date stock climb, outpacing broader market trends.

Marvell Shines Bright: A Look into Fiscal Triumphs and Projections

Marvell’s total revenue for the fourth quarter of fiscal 2024 surpassed all expectations, reaching $1.43 billion, a 1% year-on-year increase. CEO Matt Murphy attributed this success to the remarkable 38% sequential and 54% year-over-year growth in the data center end market, driven by AI technologies.

Looking ahead, although soft demand in consumer, carrier infrastructure, and enterprise networking is anticipated to affect the first quarter of fiscal 2025, management is optimistic about continued sequential growth in the data center segment. They foresee a resurgence in the second half of fiscal 2025.

Projections for the upcoming quarter peg revenue at $1.15 billion, with adjusted diluted income expected to be at $0.23 per share. However, analysts are cautious about fiscal 2025, predicting slight declines in both revenue and earnings, only to witness a robust upturn in fiscal 2026.

As Marvell’s future shines, with strong prospects in AI, the stock currently trades at 29 times forward earnings and eight times forward sales, reflecting reasonable valuations for a semiconductor stock poised for long-term growth.

Insights on MRVL Stock

Following the outstanding Q4 results, Wall Street analysts are increasingly bullish on Marvell’s stock. Stifel Nicolaus analyst Tore Svanberg maintained a “buy” rating on the stock with a price target of $86.

Overall sentiment on MRVL stock is a resounding “strong buy,” with 25 out of 28 analysts giving it the highest rating. The average price target stands at $87.78, suggesting a significant upside potential of 23.8%, while the high target price of $100 paints an even brighter picture with a potential upside of 41.1% over the next year.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.