ICON plc ICLR enters the second half of 2026 with an uneven investment profile. Customer demand signals improved in the latest quarter, but the operating model has not yet shown a clean recovery.

That split matters for investors weighing the stock. Backlog and bookings point to better commercial traction, while margins, earnings and internal controls still argue for caution.

ICON Revenue Trends Show a Mixed Reset

The latest quarter looked better on the surface than it did underneath. Revenues rose 0.9% year over year to $2.03 billion, but declined 1.9% in constant currency, showing that reported growth benefited from currency rather than a broad operating rebound.

The full-year outlook reinforces that reset. ICON’s 2026 revenue guidance remains $7.85 billion to $8.15 billion, below the $8.25 billion generated in 2025. Part of the expected decline reflects the Symphony Health divestiture, while the rest points to organic weakness.

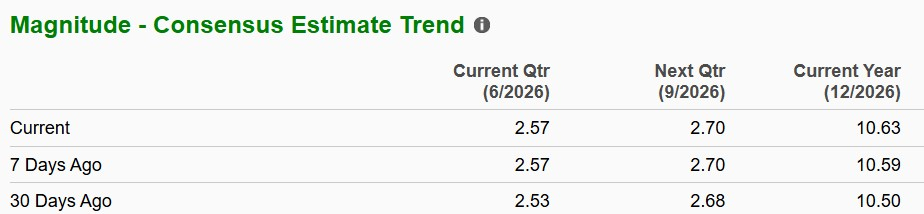

In the past 30 days, the company’s earnings per share has moved north to $10.63.

Image Source: Zacks Investment Research

ICLR Margins Remain the Core Investor Problem

Profitability is the central issue for ICLR. Adjusted EBITDA fell 20.2% year over year in the latest quarter, and adjusted EBITDA margin dropped to 15.6% from 19.8%. Adjusted earnings of $2.50 per share also declined from $3.27 a year earlier.

Management expects only gradual sequential repair. Second-quarter 2026 adjusted EBITDA margin is expected near 16%, while the full-year margin is expected near 16.5% at the midpoint of guidance. That leaves the earnings outlook sensitive to mix, project timing and cost execution.

ICON Bookings Strength Supports a Better Backdrop

The commercial picture is more encouraging. Gross bookings reached $3.26 billion, net business wins were $2.88 billion and cancellations were only $383 million. Net book-to-bill stood at 1.42X, while backlog increased 4% sequentially to $22.7 billion.

These data points matter because they suggest customer demand is stabilizing before the income statement fully reflects it. ICON also highlighted new partnerships, including a central labs arrangement with a top-five pharma customer and a midsized pharma win that displaced a large incumbent contract research organization.

IQVIA Holdings Inc. IQV remains a relevant peer because it also competes across clinical development, technology and analytics. Thermo Fisher Scientific Inc. TMO, through its PPD clinical research business, gives investors another large-scale benchmark for sponsor demand and service breadth in the contract research market.

ICLR Risks Still Cloud the 2026 Story

Investors may remain cautious because the financial reset is not the only issue. ICON disclosed revenue-recognition timing problems tied to improper adjustments from third-quarter 2023 through fourth-quarter 2024, along with related control weaknesses and certain issues extending into 2025.

The remediation effort is still underway. ICON is updating policies, adding training and strengthening controls over manual adjustments, but the timeline to fully embed those changes remains an investor-confidence risk.

The balance sheet adds another constraint. ICON exited the latest quarter with $765.2 million in cash and net debt of $2.6 billion. Net debt was 1.8X trailing adjusted EBITDA, a manageable level but one that limits flexibility if the margin recovery slips.

In the past year, ICLR’s share have risen 17.3% compared with the industry’s 13.5% growth.

Image Source: Zacks Investment Research

ICON Scores Signal Caution Over Momentum

The bottom line is that ICON has improving order flow, but the stock still needs better evidence of earnings stabilization. Backlog growth can support a more constructive setup into 2027, but 2026 remains a year of margin repair and control remediation.

The stock currently carries a Zacks Rank #5 (Strong Sell). That rank points to weak near-term earnings estimate support, which makes it harder to rely on the recent improvement in trading action alone.

ICON also has a VGM Score of D, with a Value Score of D, Growth Score of F and Momentum Score of A. The high Momentum Score fits the stock’s recent price strength, but the weak Value, Growth and VGM readings show that the broader style profile remains mixed. For investors, that combination supports a cautious view until margins and earnings visibility improve.

Research Chief Names “Single Best Pick to Double”

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners Up

ICON PLC (ICLR) : Free Stock Analysis Report

Thermo Fisher Scientific Inc. (TMO) : Free Stock Analysis Report

IQVIA Holdings Inc. (IQV) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.