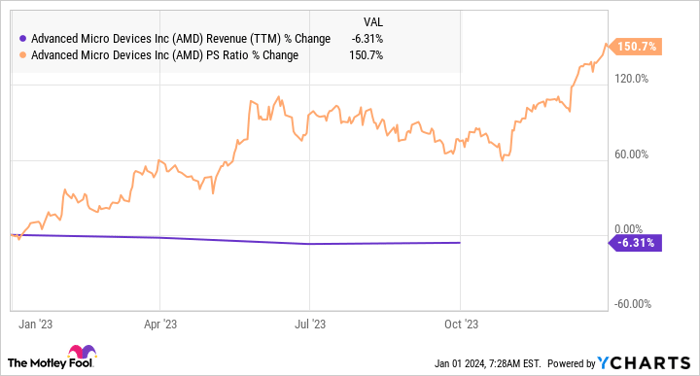

Advanced Micro Devices (NASDAQ: AMD) has been on a rollercoaster ride, with its stock soaring 127% despite a dip in revenue and earnings. As AMD’s price-to-sales multiple increased, it seems like a peculiar time to ponder if investing in the chipmaker is judicious.

AMD’s earnings are predicted to plummet by 31% in 2023 to $2.40 per share, an ominous projection considering its pricey valuation and recent financial slump. Despite these red flags, astute investors may discern pivotal catalysts that could ignite AMD’s success in 2024 and beyond.

AMD Revenue (TTM) data by YCharts.

Positive Outlook for 2024

The decline in PC sales significantly impacted AMD’s performance in 2023, with bright prospects emerging in the new year. Canalys researchers anticipate an 8% surge in PC sales in 2024 following a 12.4% downturn in 2023. This rebound will serve as a robust tailwind for AMD’s client CPU business, which suffered from the declining PC sales in 2023.

In the first nine months of 2023, AMD’s client revenue plummeted by 40% year over year, causing the company’s overall revenue to drop by 8% to $16.5 billion. The oversupply of computer processors due to weak demand for PCs forced AMD to offer discounts, eroding its margins and profitability.

However, in Q3, the client revenue surged by 42% year over year to $1.45 billion, marking a turning point signaling a potential revival for AMD.

AI Chips to Drive Growth

The growing adoption of AMD’s AI chips by industry giants like Meta Platforms, OpenAI, Oracle, and Microsoft is expected to be a key growth driver. AMD anticipates its AI chips to rake in over $2 billion in revenue in 2024, presenting a substantial opportunity for growth.

Despite Nvidia’s dominance in the AI chip space, AMD’s foray into this market is promising, especially considering its Q4 revenue forecast of $400 million from the data center GPU business. The company’s strategic alliance with a foundry partner might further bolster its prospects in the data center GPU business, potentially leading to exponential growth. Industry sources have hinted at a significant share of the AI chip supply being funneled to AMD, indicating the possibility of even more robust expansion in the data center GPU business.

AMD’s Potential Growth in AI Chip Market

AMD’s Aggressive Pricing Strategy Could Propel Growth

If AMD decides to undercut Nvidia and offers its AI GPU at $30,000, it could generate $12 billion in revenue from the data center GPU segment. With the potential to sell 400,000 AI GPUs in 2024, AMD could gain a significant edge over Nvidia in the market.

Forward Outlook: Favorable for Investment

According to estimates, AMD’s revenue and earnings are projected to exhibit strong growth in 2024 and 2025. The company’s growth trajectory is anticipated to outpace current analyst expectations, making it an attractive investment option.

|

Year |

Revenue estimate (in $billion) |

Year-over-year change (%) |

Earnings per share estimate |

Year-over-year change (%) |

|---|---|---|---|---|

|

2023 |

$22.7 |

-4% |

$2.65 |

-24% |

|

2024 |

$26.5 |

17% |

$3.83 |

45% |

|

2025 |

$31 |

17% |

$5.16 |

35% |

Source: YCharts and Yahoo! Finance

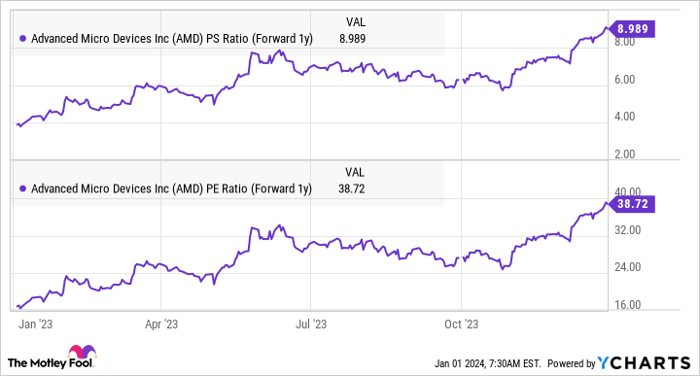

AMD’s forward earnings and sales multiples are relatively enticing compared to the trailing multiples mentioned earlier. This reflects a positive market sentiment towards AMD’s future growth potential.

AMD PS Ratio (Forward 1y) data by YCharts.

Potential for Market Reward and Investment

AMD’s accelerated growth, coupled with its significant opportunity in the AI chip market, presents an attractive investment opportunity. Savvy investors seeking growth stocks to capitalize on the proliferation of AI and the resurgence of the PC market should consider adding AMD to their portfolios before its value soars further.

Consideration Before Investment

Before investing in AMD, it’s essential to weigh the potential for growth against market dynamics and competition. The decision should be founded on a comprehensive understanding of AMD’s position in the industry and its potential for future gains.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Meta Platforms, Microsoft, Nvidia, and Oracle. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.