Despite broader market apprehensions regarding valuations, select individual stocks like Ford appear to present compelling valuations. With mid-single-digit price-to-earnings multiples, Ford is viewed as a deep-value stock. Additionally, boasting a 5% dividend yield, the Detroit-based automaker’s dividend payout surpasses that of the average S&P 500 Index constituent by over threefold.

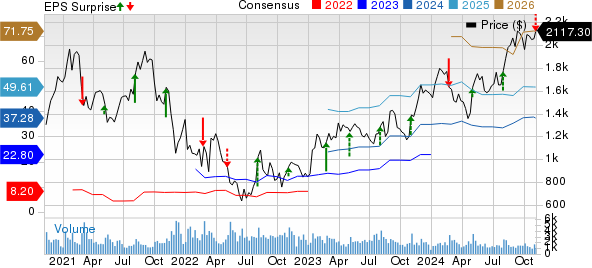

While Ford’s stock has struggled to keep pace with the market in 2024, experiencing a 3.9% decline amidst record highs in broader indexes, the company’s shares have endured a significant 30% depreciation over the past decade.

Despite Ford’s consistent underperformance, the stock continues to see declining prices, prompting concerns about it being a potential “value trap.” Nonetheless, there is a belief that the stock has limited downside from current levels and could be viewed as an undervalued asset worthy of acquisition at its current valuations.

Delving into Ford’s Underperformance

The automotive industry is navigating a turbulent phase, characterized by legacy automakers such as Ford and General Motors investing substantial sums in electric vehicle (EV) infrastructure, only to encounter weaker-than-expected demand.

This situation has led to excess capacity within the industry, resulting in substantial losses in the EV sector. Ford, particularly transparent about its EV business, recorded a staggering pre-tax loss of $4.7 billion through its Ford Model e segment in 2023. The company foresees these losses widening to between $5 billion and $5.5 billion in 2024.

Originally anticipated as a lucrative venture, Ford’s Model e has transformed into a significant drag on its overall performance, eroding profits generated by other segments such as Ford Blue and Ford Pro.

Evaluating Ford’s Stock Forecast

Wall Street analysts remain relatively cautious on Ford stock, offering a consensus rating of “Moderate Buy.” Among the 19 analysts covering the stock, only seven label it as a “Strong Buy,” while eight rate it as a “Hold,” and three more as a “Strong Sell.”

With a mean target price of $13.80, Ford’s stock is positioned to rise by nearly 18% from current prices, while the Street’s highest target price of $21, offered by Bank of America, implies an increase of over 79%.

Assessing Ford’s Undervaluation

Trading at a next 12-month (NTM) PE multiple of 5.9x, Ford’s stock valuation has raised discussions regarding its modest multiples. During Ford’s Q1 earnings call, Morgan Stanley’s analyst Adam Jonas highlighted that the company ranked 491st among S&P 500 index companies in terms of PE multiples.

CEO Jim Farley attributed the subdued stock performance to EV losses, labeling it as an industry-wide issue. Ford projects its Ford Pro commercial segment to generate adjusted pre-tax profits ranging from $8 billion to $9 billion in 2024, while anticipating Ford Blue’s internal combustion engine (ICE) business to yield adjusted pre-tax margins of $7 billion to $7.5 billion.

With Ford Pro anticipated to have a comparable market cap to the current consolidated value, the company is expanding its hybrid portfolio and intends to introduce hybrid versions across its product range, providing flexibility to adapt to market shifts.

Predicting Ford’s Dividend Trend

While both Ford and GM exhibit healthy free cash flows, they are employing divergent strategies in capital allocation. GM focuses on share repurchases with a recent $6 billion buyback announcement, whereas Ford intends to allocate 40%-50% of its free cash flows towards dividends, supplemented by special dividend payments.

In conclusion, despite Ford’s lackluster price performance, there is optimism regarding its potential for revaluation in the medium term. Investors can meanwhile relish the robust dividend yield, coupled with the prospect of additional special dividends, as the company aims to deliver significant returns to its shareholders.