Tech stocks faced adversity in 2022 amid challenging macroeconomic conditions, but surged into 2023 on the winds of the artificial intelligence (AI) boom. Most AI tech stocks have bolstered their positions by merging AI into their products to stay competitive in a cutthroat industry.

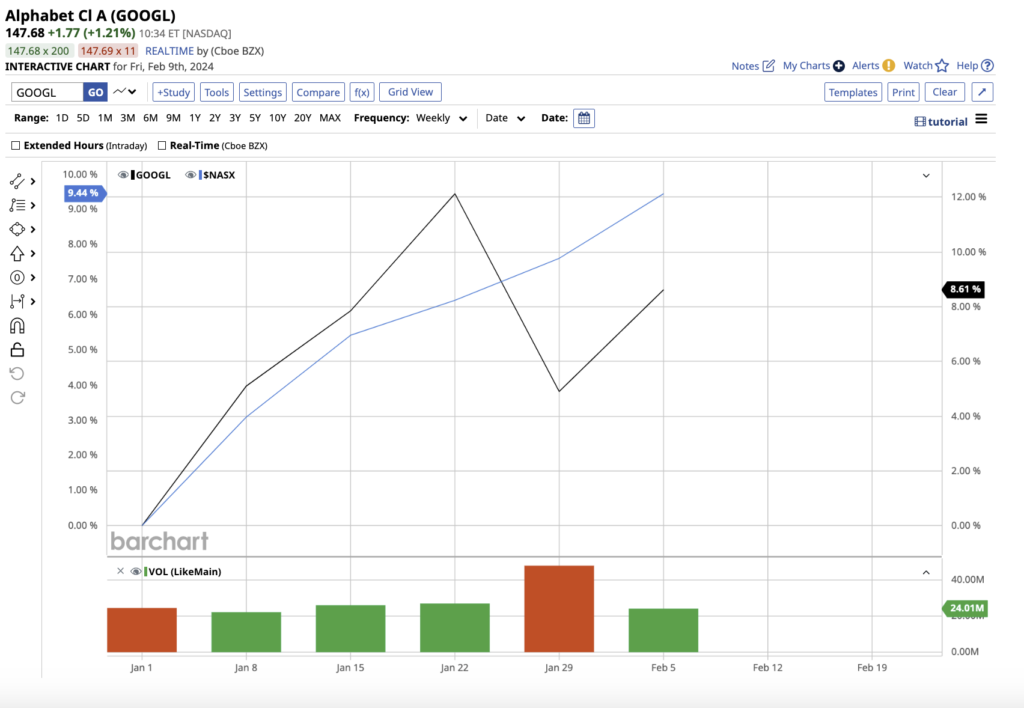

Alphabet (GOOGL) and Advanced Micro Devices (AMD) stand out as top growth picks for the year ahead. In 2023, both companies outperformed the Nasdaq Composite with Alphabet’s stock gaining 58% and AMD’s shares surging 127%.

The Case For Alphabet Stock

Since 2017, Alphabet has been integrating AI into its diverse product offerings, such as Gmail, Photos, and Maps. As AI technology advances, the company plans to unveil even more sophisticated products to its consumers. Despite GOOGL’s 6.7% YTD surge, the stock remains 3% below its all-time high.

Alphabet’s flagship Google Search continues to reign over the search engine market with an estimated 92% share. Notwithstanding challenges from the Department of Justice and its rival Microsoft (MSFT) questioning its monopoly last year, Google Search’s revenue rose by 8% year-over-year to $175 billion in 2023.

Another key growth driver for Alphabet is Google Cloud, which ranks third in the global cloud computing market. Cloud revenue escalated by 26% YoY, amounting to $33 billion in 2023. YouTube ad revenue also surged 7.7% to $31.5 billion over the year.

CEO Sundar Pichai expressed satisfaction with the company’s performance, stating, “We are pleased with the ongoing strength in Search and the growing contribution from YouTube and Cloud. Each of these is already benefiting from our AI investments and innovation. As we enter the Gemini era, the best is yet to come.”

Alphabet boasts robust financials with $110.9 billion in cash, cash equivalents, and marketable securities, paired with $13.2 billion in long-term debt. Moreover, it reported a free cash flow of $69.5 billion at the end of the quarter.

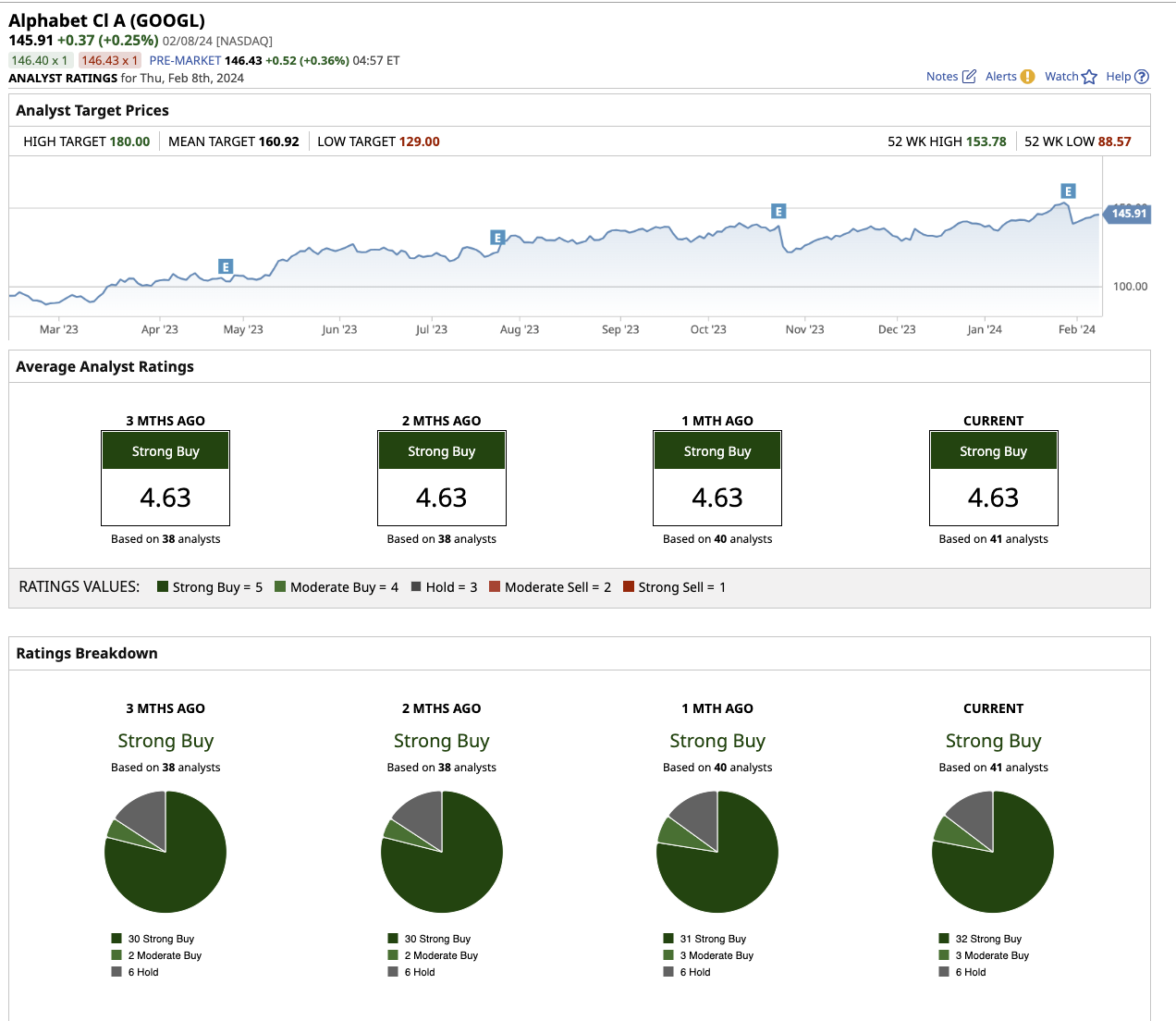

Of the 41 analysts covering Alphabet stock, 32 rate it as a “strong buy,” three as a “moderate buy,” and six as a “hold.” With an average price target of $160.92, Wall Street foresees an 8% potential upside in the next 12 months, with the highest target set at $180.

Analysts anticipate an 11.4% revenue growth and a 16.1% earnings growth for Alphabet in 2024. With a forward price-to-earnings (PE) ratio of 21, Alphabet appears to be a reasonably priced high-growth stock to consider amidst the current decline.

The Case for Advanced Micro Devices Stock

Although Nvidia (NVDA) has long been dominant in the semiconductor space, AMD has made significant strides in cementing a strong market position. The company’s fundamentals improved notably as the demand for its graphic processors surged last year.

AMD’s shares have climbed 17% YTD, outperforming the S&P 500 Index’s 5.4% gain.

AMD’s data center segment is witnessing a strong recovery. In the fourth quarter, the segment’s revenue soared by 38% YoY to $2.3 billion, driven by expanding customer adoption of AMD Instinct GPUs and 4th Gen AMD EPYC CPUs. Meanwhile, AMD’s client segment sales skyrocketed by 62% to $1.5 billion, supported by an increase in demand.

AMD’s Mixed Q4 Performance

The fourth quarter brought mixed results for Advanced Micro Devices (AMD). While the company reported a 10% year-over-year increase in total revenue to $6.2 billion and a substantial rise in diluted earnings per share (EPS) to $0.41, sales in the gaming segment saw a significant 17% decrease. Additionally, the embedded segment witnessed a 24% decline in sales during the same period. Despite these challenges, management remains optimistic about the long-term growth prospects, particularly in the AI and embedded segments.

AI Segment Expansion

In a bid to bolster its AI capabilities, AMD made strategic acquisitions, including the AI software leader Mipsology and open-source AI software expert Nod.ai. These acquisitions align with the company’s vision to strengthen its AI software ecosystem and capitalize on the increasing demand for high-performance graphic processors in the AI era. The expansion into the AI space is expected to support AMD’s future growth trajectory as the industry continues to evolve.

Analyst Predictions and Market Outlook

Despite the mixed performance in Q4, analysts foresee a positive outlook for AMD in 2024. They anticipate a 13.8% increase in revenue and a significant 37.7% rise in earnings year-over-year. This positive forecast reflects the market’s confidence in AMD’s ability to navigate through the current headwinds and capitalize on future growth opportunities.

Wall Street has maintained a bullish stance on AMD, with the majority of analysts assigning a “strong buy” rating to the stock. Out of the 33 analysts covering AMD, 27 recommend it as a “strong buy,” while one suggests a “moderate buy,” and five advise a “hold.” The average target price for AMD stands at $184.37, indicating a potential upside of 6.8% over the next 12 months. Furthermore, the high target price of $270 implies a substantial 56% upside from the current levels, reflecting the optimistic long-term sentiment among analysts.

Source: www.barchart.com

Source: www.barchart.com

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.