The semiconductor industry, often referred to as the chip sector, serves as the backbone of contemporary technological progress. Within this domain, Nvidia, AMD, and Intel stand as pivotal players, molding the computing and artificial intelligence (AI) arena. A profound analysis using TipRanks’ Stock Comparison tool has been conducted to shed light on the stock with the most promising value proposition in this trio.

Nvidia: The Master of AI

At the nucleus of the industry, Nvidia (NVDA) radiates as the powerhouse orchestrating the AI revolution. With its potent chips fueling cutting-edge AI systems and data centers, Nvidia enjoys a substantial lead over its competitors. Over a decade of honing its Graphics Processing Units (GPUs) and accompanying software has bestowed Nvidia with an unparalleled full-stack offering prowess.

The recent performance tumult on Nvidia’s stock stirred concerns among stakeholders. Plunging into bear territory post a staggering decline wiping around $300 billion off its market cap, Nvidia underwent a 24% stock slide from its June 20 high, puncturing through its 50- and 100-day moving averages. Multiple factors, such as post-earnings adjustments, the semiconductor sector’s lackluster September showing, and the emergence of reports hinting at OpenAI’s internal chip development, contributed to this downturn.

Add to the mix the Department of Justice’s antitrust probe subpoena rumor, sternly refuted by Nvidia itself, and the volatile AI sentiment; investor optimism towards Nvidia has subtly waned.

Evaluating Nvidia’s Stock Performance

Despite the whirlwind, Nvidia’s earnings revisions uphold an optimistic tone. The preceding 90 days documented a tally of 31 upward adjustments versus merely six downwards revisions, underscoring durable faith in the company’s capacity for outperformance. With a 38.7x forward earnings multiple and a favorably poised price-to-earnings-to-growth (PEG) ratio at 1.03, Nvidia’s stock appears compelling within the technology realm.

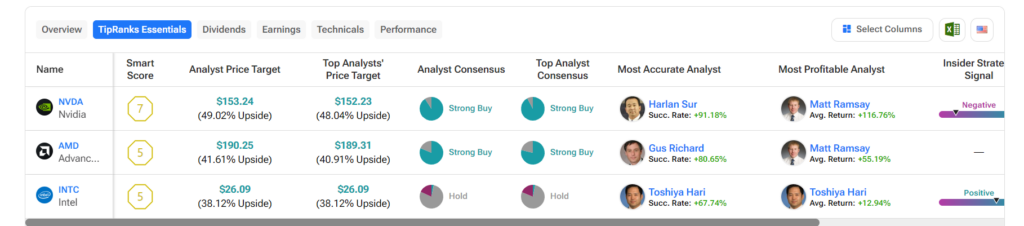

The analyst consensus remains predominantly bullish, endorsing Nvidia as a Strong Buy following 39 Buy recommendations, four Holds, and zero Sells within the recent quarter. Anticipated at $151.79, the average Nvidia stock price target projects an impressive 47.61% upward potential.

AMD: The Underdog Nipping at Nvidia’s Heels

AMD (Advanced Micro Devices) emerges as a formidable contender to Nvidia’s stronghold in the AI segment, albeit commanding a smaller market share. While Nvidia claims 80% of the AI accelerator market, AMD is swiftly positioning itself as a competitive alternative. Opting for a hardware efficiency-driven agenda over Nvidia’s holistic approach, the company’s strategic trajectory diverges.

Positioning its latest Instinct MI300x with purported latency and throughput superiority of 40-60% over Nvidia offerings, AMD has sparked fervent competition. Yet, disparities persist in software ecosystems, even though recent acquisitions point towards AMD’s stride in expanding its AI toolkit.

AMD’s revenue boomed by 80% YoY to $2.3 billion in Q1 2024, buoyed by the burgeoning AI and data center module demand. This ascension, however, veils the Gaming Segment’s slump, witnessing a distressing 59% revenue plummet YoY to $648 million.

Assessing AMD’s Stock Potential

Amid the churn, AMD’s stock witnessed periodic retreats this year, aligning with broader market corrections in early September. Presenting itself as a more economical option at a glance, AMD’s 90-day revision trends document 26 downward adjustments juxtaposed with only nine upward revisions.

Favorable grounds surface with AMD trading at a 41.6x forward earnings multiple, complemented by a sub-unity PEG ratio of 0.97. This humble PEG ratio typically presages undervalued circumstances, a rare phenomenon in the tech domain. Reinforcing analyst confidence, TipRanks designates AMD as a Strong Buy, premised on 26 Buy ratings, six Holds, and no Sells over the past quarter. An average AMD stock price target of $190.25 hints at a promising 41.61% upswing.

Intel: Navigating Choppy Waters

Intel (INTC) navigated hazardous terrain in recent times, with some industry observers questioning its prospects to reclaim semiconductor dominion. Intel’s tribulations trace back nearly a decade. Historically lauded for enhancing chip-making processes, the company ran into innovation impediments circa 2014.

Initially imperceptible repercussions escalated during the pandemic, unmasking Intel’s technological frailties. Consequently, Pat Gelsinger’s appointment as CEO heralded the audacious “five nodes in four years” blueprint, aiming to fast-track technology progression and close the competitive gap.

Undoubtedly, Intel’s strategic recalibration is a protracted expedition, its culmination premature and speculative at this developmental juncture.

Evaluating Intel’s Stock Outlook

Today’s woes stem from yesteryears’ misjudgments. Trading at a 75.4x forward earnings multiple and bearing a 1.88 PEG ratio, Intel’s stock appears precariously perched. These metrics prognosticate plausible further declines, but hinge on the efficacy of present-day decisions to resuscitate past grandeur.

Analyst sentiments diverge on Intel, labeled as a Hold on TipRanks based on a single Buy, 26 Holds, and five Sells in the preceding quarter. The average Intel stock price target of $26.09 suggests a 38.12% prospective escalation.

The Verdict

In this labyrinth of choices, which stock heralds the paramount value proposition? My inclination veers toward Intel, draped in speculative allure post its recent trajectory. However, exuberance envelopes Nvidia and AMD, ensconced in discounted stock valuations alongside enticing PEG ratios.

Disclosure

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.