The late, great Charlie Munger was a world-class investor. Warren Buffett’s right-hand man had an affinity for Costco Wholesale, which made countless investors rich with a simple business model centered around charging customers a membership fee to shop at a store they loved.

Shares haven’t slowed much, either. The stock has returned over 570% over the past decade, more than doubling the S&P 500.

So, I say this with the utmost respect: You can do better.

E-commerce giant Amazon (NASDAQ: AMZN) has not only done far better in the past, with its stock returning 1,200% in the last 10 years besides returning a staggering 193,000% since it went public in 1997 — the company is better placed to outperform Costco over the next decade as well.

Here is why Amazon is the blue chip retail stock you need to own.

Why Costco could slow down…

Costco is a world-class business, but the stock isn’t perfect. It is one of the world’s largest retailers, with 76.2 million paid members and $254 billion in annual revenue. The business works on razor-thin profit margins since low prices are part of the appeal to shoppers. In reality, most of the company’s profit comes from the membership fees it charges to shop at its stores.

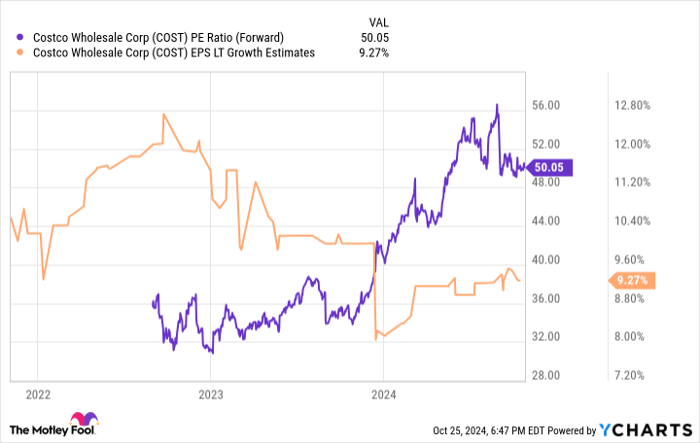

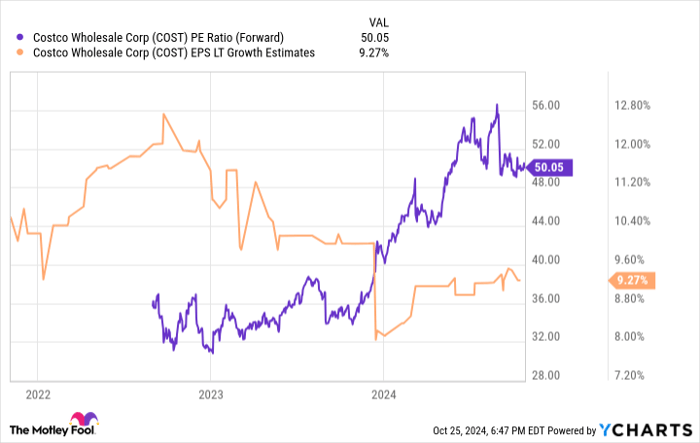

So, its earnings growth is somewhat tied to how fast it can grow its membership base. It can also raise its fees, but it doesn’t like to do that — management just raised them for the first time in seven years in September. Costco’s paid customer count increased 7.3% year over year in its most recent quarter. Over the long term, analysts estimate Costco will grow its earnings by an average of 9.3% annually:

COST PE ratio (forward) data by YCharts; EPS = earnings per share.

That’s not much growth for a stock that has risen to a price-to-earnings (P/E) ratio of 50. Costco is great, but I’m skeptical the stock will maintain that valuation. A reasonable price/earnings-to-growth ratio (PEG) for a quality stock might be as high as 2 to 2.5; today, Costco’s is 5.4. In such a case, the stock is vulnerable to a sharp decline or could stay flat while the business catches up to the stock.

…and why Amazon won’t

Amazon’s retail business is like Costco’s online twin. It also works on slim profit margins. Like Costco, it monetizes its retail business via a paid membership. You don’t need a Prime membership to shop on Amazon, but the perks have convinced over 200 million members to join.

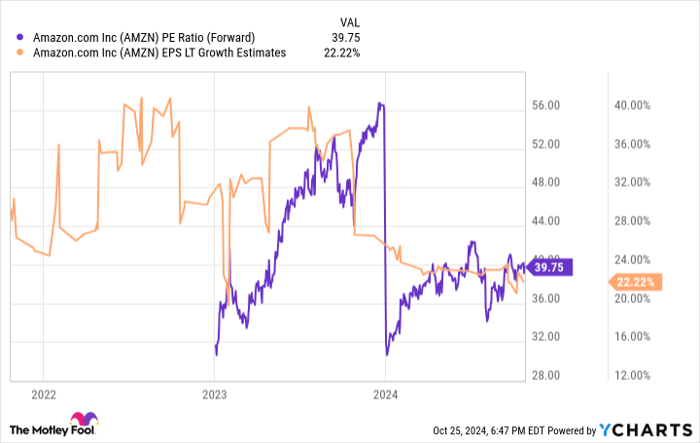

There is a drastic difference, though, in Amazon stock. The stock trades at a forward P/E of just under 40, while analysts estimate the company can grow earnings by more than 22% annually over the long term. That’s a PEG of 1.8, well within that reasonable range I outlined above.

Even if earnings growth happens at a more modest 16%, accounting for uncertainty, the PEG ratio would then be just 2.5 — nothing alarming for a growing business.

AMZN PE ratio (forward); data by YCharts.

Costco is growing more slowly than Amazon, yet the stock is more expensive. This probably won’t last forever, which is why Amazon is the better stock for the future.

The long-term prospects look tantalizing

It’s worth asking why Amazon is growing so much faster than Costco. The answer boils down to two reasons.

First, Amazon is America’s largest online retailer by a country mile. It owns roughly 40% of e-commerce in the United States. Consumers are gradually doing more of their shopping online. Approximately 16% of retail is online today, up from 4.2% in 2010. As that increases, the company will naturally benefit and ride that trend to growth.

Second, Amazon has expanded its business well beyond retail. Its cloud platform, Amazon Web Services, has become theglobal marketleader in cloud computing, which — similar to e-commerce — positions it to enjoy the tailwinds of long-term industry growth. More companies are migrating to the cloud, and the emergence of artificial intelligence (AI) will only add to that. That doesn’t even get into media and advertising, Amazon’s fastest-growing business.

The company has arguably made more people millionaires than any other stock over the past 30 years. Remarkably, it still looks like there’s plenty left in the tank. Costco is no slouch, but Amazon is the better buy, and it’s not even close.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,492!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,204!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $409,559!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 28, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Costco Wholesale. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.