Qualcomm, the seasoned mobile-chip powerhouse listed on NASDAQ under QCOM, has surprisingly emerged as a suitor’s dream in the volatile vortex of 2024. Weathering the tumult of a post-pandemic gadget spree, Qualcomm’s shares have surged to unprecedented altitudes, boasting a stalwart 40% climb since the year’s advent.

The rationale underpinning this meteoric rise is anchored in Qualcomm’s clever cultivation of novel consumer vistas, ushering in winds of fortune that swirl with promise. While the smartphone sector might languish, Qualcomm’s forays into burgeoning markets spell an uptick in profitability, rendering the stock a veritable treasure trove of potential.

The Acceleration of the Automotive Sector and the Revving of PC Sales

Resurrecting from the ashes of uncertainty, Qualcomm now revels in the revitalization of the smartphone domain thanks to the buoyant demand for its premium 5G connectivity chips. Spearheading Qualcomm’s revenue upswing, these high-end chips fetch higher prices, outshining the market’s lackluster performance.

But the plot thickens. Qualcomm’s long-slumbering PC venture promises a renaissance with the impending launch of its Snapdragon X Elite laptop chips. Crafted for Microsoft Windows laptops on the storied Arm Holdings architecture, akin to Apple’s lauded MacBook lineup, this venture unearths a fresh territory ripe for Qualcomm’s conquest. A domain traditionally lorded over by Intel and AMD, Qualcomm’s potential market incursion drips with promise, offering a lucrative pedestal for growth akin to its erstwhile automotive exploits.

Qualcomm’s revenue is starting to look very different from historical norms. Source: Qualcomm.

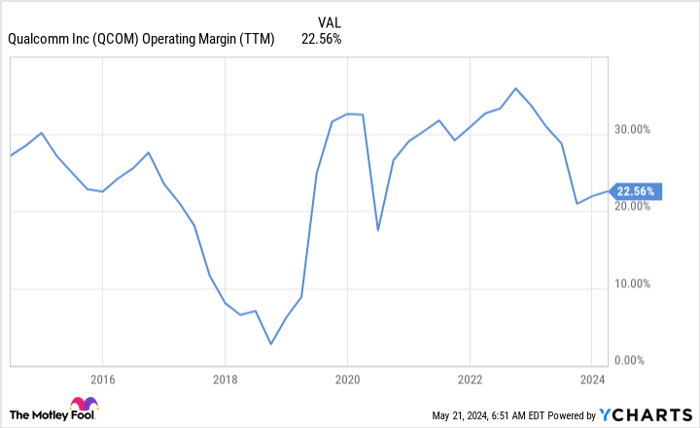

The Coveted Corner of Margins

Amidst the cyclical undulations of the smartphone realm, Qualcomm boasts a resilient business model that perennially delivers robust profitability. As the consumer expenditure landscape convalesces from the pandemic-induced convulsions and rate hikes, Qualcomm’s profit margins are poised to thrive.

Moreover, Qualcomm’s profit reservoirs face sustenance from the burgeoning PC and automotive chip sectors. As these ventures yield bountiful returns, Qualcomm’s margin coffers are destined for augmentation, setting the stage for brighter days.

Data by YCharts. TTM = trailing 12 months.

While Qualcomm may not scale the semiconductor Olympus at breakneck speeds, the confluence of elevated ASPs in smartphone chips and nascent growth channels like Windows laptops and automotive chips hints at a modest low-teens upswing in earnings per share (EPS) over the ensuing years.

A bargain at 27 times trailing-12-month EPS or 18 times free cash flow, Qualcomm morphs into an irresistible proposition of enduring worth.

Is Qualcomm Worth a $1,000 Gamble?

Prior to plunging into Qualcomm’s stock realm, pause to ponder:

The celebrated minds at Motley Fool Stock Advisor have pinpointed 10 red-hot stocks, visions of meteoric returns shimmering in their gaze… with Qualcomm conspicuously absent from the roster. A tantalizing prospect looms, promising eye-popping returns in the forthcoming era.

Reflect on the historic moment when Nvidia graced this list in 2005 – a $1,000 dalliance then would have swelled to a staggering $635,982 now!*.

Stock Advisor bequeaths a roadmap to prosperity, guiding investors through the labyrinth of portfolio construction, interspersed with analyst insights and bi-monthly stock revelations. Since 2002, Stock Advisor has eclipsed the S&P 500’s return, transcending mere investment sagas to apocryphal tales of boundless returns*

*Stock Advisor returns as of May 13, 2024