Once considered uninvestable, JD.com (JD) and other China-based businesses are experiencing a significant shift in sentiment. This change comes on the heels of China’s aggressive monetary-policy moves, signaling a potential boon for JD stock in the upcoming quarters. With a focus on income growth and reasonable valuation, JD.com presents an enticing investment opportunity amidst the evolving Chinese economic landscape.

JD.com, a formidable e-commerce player in China, despite trailing behind Alibaba (BABA) in size, boasts a substantial market capitalization of approximately $62 billion. Despite a tumultuous stock performance over the past year resembling a rollercoaster ride, JD.com is showing signs of resurgence, offering investors a promising entry point into the revitalizing Chinese economy.

China’s Stimulus Impact on JD.com

China’s recovery post-pandemic has been turbulent, with cyclical businesses like Alibaba and JD.com navigating challenging conditions. However, a recent wave of substantial monetary stimulus from the Chinese government has sparked optimism. This support bodes well for JD.com as a potential boost in business activity could propel the company’s financial performance forward.

The surge in China’s technology stocks, resulting in the best week since 2008, signifies a significant shift in global investors’ perceptions of Chinese investments. The People’s Bank of China’s injection of an RMB800 billion lending pool into the capital markets is reshaping the narrative around Chinese businesses, making them more appealing to investors. JD.com stands to benefit from the substantial liquidity support from the government, potentially driving e-commerce sales and income growth in the near future.

JD.com’s Robust Income Growth

JD.com stands out among Chinese stocks due to its robust financial foundation. With $28.8 billion in cash reserves and minimal debt, the company exhibits financial stability. Furthermore, JD.com’s impressive income growth, with a nearly 100% year-over-year increase in diluted net income per ADS in the second quarter of 2024, showcases its resilience in navigating challenging economic conditions. Having surpassed earnings estimates for over 15 consecutive quarters, JD.com’s performance is likely to be bolstered further by the government’s financial support initiatives.

JD.com’s Attractively Valued Position

JD stock’s recent uptick following China’s stimulus announcements indicates further upside potential. With a reasonable price-to-earnings (P/E) ratio, JD.com presents an appealing opportunity for value-conscious investors eyeing U.S.-listed Chinese stocks. Calculating a trailing 12-month adjusted P/E ratio of 10.39x, below the sector median and JD.com’s historical average, the stock appears undervalued. Value seekers are advised to consider JD.com for potential growth in their portfolios.

Analyst Perspectives on JD Stock

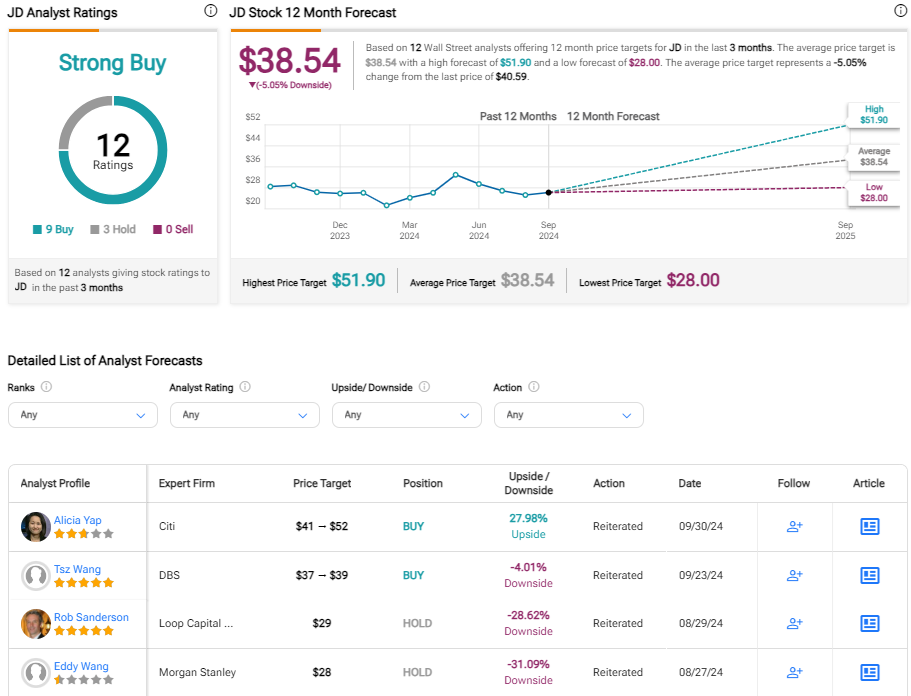

Wall Street analysts view JD.com favorably, with a Strong Buy rating based on nine Buys and three Holds in the past three months. The absence of Sell ratings and an average price target of $38.54 underpin confidence in JD.com’s future performance. Analyst sentiment aligns with the positive outlook for JD.com stock in the current market landscape.

Should Investors Consider JD Stock?

Amidst the recent surge in share price, JD.com remains reasonably valued, supported by a trajectory of increasing profitability. Positioned as a cyclical e-commerce player set to benefit from government stimulus measures, JD.com presents a compelling investment case. While not devoid of risks, the Strong Buy rating from analysts underscores the consensus on JD.com’s promising outlook for long-term investors.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.