Alphabet GOOGL shares have returned 7.4% year to date (YTD), outperforming the Zacks Computer & Technology sector’s 4.1%. The company’s prospects are expected to benefit from its growing AI-powered search capabilities and significant investments in cloud computing. However, capacity constraints, despite the improving pace of server deployments and data center construction, are expected to hurt Alphabet’s prospects in 2026. This, along with higher depreciation expenses and related data center operations costs, including energy, is expected to hurt profitability. Higher sales and marketing expenses are expected to keep the margins under pressure. So, what should investors do with GOOGL shares?

GOOGL Suffers From Stiff Competition & Higher Capex

Alphabet is facing stiff competition in the cloud computing space from Microsoft MSFT and Amazon AMZN. According to Synergy Research Group’s fourth-quarter 2025 data, Amazon maintained a strong lead in the market, though Microsoft and Alphabet’s Google continued to achieve substantially higher growth rates. Amazon, Microsoft and Alphabet’s market share were roughly 28%, 21% and 14%, respectively. In the search domain, Google continues to dominate with a roughly 89.98% share, followed by Microsoft’s Bing, with a 5.01% share, per the latest data from StatCounter. In the consumer technology market, Alphabet continues to face stiff competition from Apple AAPL.

Investor skepticism over GOOGL’s ability to monetize its AI-infused services, given the huge capital expenditure guidance, which is now pegged between $175 billion and $185 billion for 2026, has been a headwind. Most of this spending is marked for building AI and cloud infrastructure, including data centers, chips and servers for Gemini and cloud growth. Although Alphabet generates considerable cash flow ($164.71 billion on a trailing 12-month basis at the end of fourth-quarter 2025), this steep increase in capital expenditure is expected to squeeze free cash flow ($73.27 billion on a trailing 12-month basis at the end of fourth-quarter 2025).

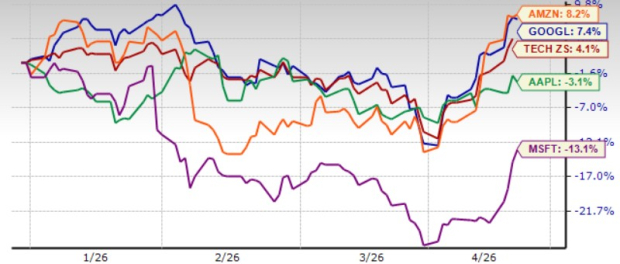

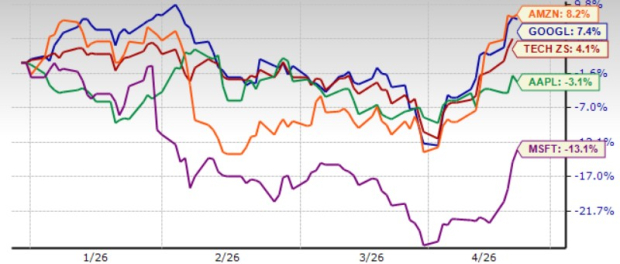

GOOGL shares have outperformed peers, including Apple and Microsoft, year to date, but lag Amazon. Shares of Apple and Microsoft dropped 3.1% and 13.1%, respectively, while Amazon returned 8.2%.

GOOGL Stock’s Price Performance

Image Source: Zacks Investment Research

2026 Earnings Estimate Revisions Steady for GOOGL Stock

The Zacks Consensus Estimate for 2026 earnings is pegged at $11.53 per share, unchanged over the past 30 days, indicating 6.7% year-over-year growth. The consensus mark for 2026 revenues is pegged at $409.43 billion, indicating 19.4% year-over-year growth.

Alphabet Inc. Price and Consensus

Alphabet Inc. price-consensus-chart | Alphabet Inc. Quote

The consensus mark for first-quarter 2026 earnings is pegged at $2.63 per share, down by a penny over the past 30 days, suggesting a 6.4% decline year over year. The Zacks Consensus Estimate for first-quarter 2026 revenues is pegged at $92.17 billion, implying 20.5% year-over-year growth.

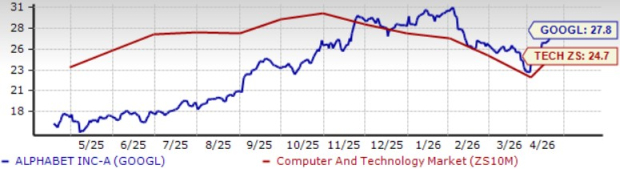

Alphabet Shares Are Overvalued

GOOGL shares are overvalued, as suggested by a Value Score of D. The Alphabet stock is trading at a forward 12-month price/earnings (P/E) of 27.8X compared with the broader Zacks Computer & Technology sector’s 24.7X.

Alphabet shares are trading at a premium compared with Microsoft, shares of which are trading at a P/E multiple of 22.83. However, GOOGL shares are trading at a lower multiple compared with Apple’s 29.62 and Amazon’s 30.35.

GOOGL Stock’s Valuation

Image Source: Zacks Investment Research

AI Push Boost GOOGL’s Search & Cloud Business

Alphabet has been actively embedding AI, especially within Search, to enhance user experience, provide better AI-focused features and consequently improve ad performance. The company integrated Gemini 3 directly into AI Mode in Search. Upgradation of AI Overviews to Gemini 3 is offering users a best-in-class AI response at the top of the search results page. GOOGL has made the transition from an AI overview to a conversation in AI Mode completely seamless. The company has expanded Search Live globally to all languages and locations where AI Mode is available. This now allows people in more than 200 countries and territories to have interactive conversations with Search in AI Mode, using both voice and camera. Expanding AI features is driving up user experience as well as engagement.

Google Cloud is benefiting from strong Gen AI adoption due to leading models, including Gemini, Imagen, Veo, Chirp and Lyria. Google Cloud’s expanding enterprise clientele has been a key catalyst. More than 120,000 enterprises use Gemini, including AI companies like Lovable and Open Evidence and global enterprises like Airbus and Honeywell. Moreover, 95% of the top 20 and over 80% of the top 100 SaaS companies use Gemini, including Salesforce and Shopify. Alphabet’s expanding AI infrastructure is helping it win enterprise clients. GCP’s prospects remain robust, driven by strong demand for enterprise AI infrastructure, including TPUs and GPUs, enterprise AI solutions driven by demand for the latest Gemini and other AI models, and other services, including cybersecurity and data analytics.

Conclusion

Alphabet is benefiting from accelerated growth across AI infrastructure, Google Cloud, and Search. However, stiff competition in cloud computing and higher capex have been concerning. GOOGL’s stretched valuation is a concern.

Alphabet currently has a Zacks Rank #3 (Hold), suggesting that investors should wait for a more favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market’s next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don’t build. It’s just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>

Amazon.com, Inc. (AMZN) : Free Stock Analysis Report

Apple Inc. (AAPL) : Free Stock Analysis Report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Alphabet Inc. (GOOGL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.