In the world of Chinese e-commerce, the clash between Alibaba (BABA) and PDD Holdings (PDD) is a tumultuous one, filled with ups, downs, and twists. These behemoths of online retail have captured the imagination of investors worldwide, each with its own unique strengths and weaknesses. Let’s delve into the heart of the matter to determine which of these titans may be the more gratifying prospect for those seeking to navigate the labyrinth of Chinese e-commerce.

The Tale of Two Giants: A Deeper Dive

The narrative of Alibaba and PDD unfolds against the backdrop of China’s ever-evolving e-commerce landscape. Alibaba, with its multifaceted ecosystem spanning platforms like Tmall and Taobao, casts a wide net both domestically and globally. In contrast, PDD’s claim to fame is its discount-driven e-commerce platform Pinduoduo, bolstered by its international venture, Temu.

Market performance reveals a stark contrast between the two giants. While Alibaba has weathered a 5% year-to-date increase in its stock value juxtaposed against an 18% decrease over the last year, PDD has experienced a reverse trajectory with a 12% decrease this year coupled with a 43% surge in the past 12 months.

The Valuation Conundrum

Despite their divergent stock trajectories, Alibaba and PDD share comparable valuations, prompting a closer examination of their price-to-earnings (P/E) ratios. Situated within a realm of unprofitability that typifies much of the Chinese online retail sector, these e-commerce giants defy conventional industry benchmarks. Instead, their valuations are best gauged through a price-to-sales (P/S) lens, with the Chinese e-commerce industry perched at a P/S ratio of 1.2x, primed against a three-year average of 1.4x.

Unpacking Alibaba (NYSE:BABA)

Alibaba emerges as a compelling proposition, boasting a P/E of 18.4x and a P/S of 1.3x, placing it in an attractive valuation sphere. Notably, the company’s forward P/E of 8.8x signals substantial projected earnings growth, painting a bullish picture for savvy investors.

Alibaba’s evolution has drawn parallels to the journey of Amazon, once revered as a growth stock before pivoting toward a more mature phase. With a burgeoning cloud business echoing Amazon’s trajectory, Alibaba’s strategic maneuvers in cloud revenue expansion and platform revitalization set the stage for enhanced growth prospects.

While the specter of diminished revenue growth looms following an 8% year-over-year increase in overall revenue for Alibaba, the allure of a potentially resurgent growth narrative underpins its current valuation appeal. Market positioning at historical P/E low points further accentuates Alibaba’s investment allure, despite recent income fluctuations stemming from investment activities.

The nuanced interplay of expectations versus performance underscores the risk associated with Alibaba’s stock, juxtaposed against the meteoric rise of Amazon in the U.S. domain. The tantalizing prospect of heightened sales growth in China’s expansive market beckons, buttressing Alibaba’s investment case with a blend of promise and peril.

The Enigmatic PDD Holdings (NASDAQ:PDD)

PDD’s narrative unfolds against a backdrop of intriguing contrasts, with a P/E ratio of 17x aligning it closely with Alibaba’s valuation vista. However, a P/S ratio of 4.4x hints at potential overvaluation, albeit against a backdrop of extraordinary sales-driven growth endeavors.

Steadfastly embracing its growth stock epithet, PDD’s meteoric revenue explosion at 90% in 2023, though tempered by a narrower revenue base than Alibaba, underscores its investment magnetism. Despite a forward P/E of 10.5x auguring well for future growth trajectories, regulatory shadows linger over PDD’s operational landscape.

The regulatory undercurrents in North America, specifically around Temu’s marketplace operations and its TikTok affiliation, evoke cautionary tones in PDD’s investment narrative. Regulatory clarity and financial transparency are the dual pillars shaping investor sentiment around PDD, where Temu’s ascension to prominence heralds both promise and regulatory reverberations.

The road ahead for PDD remains intertwined with the labyrinthine realm of regulatory scrutiny and market evolution, perhaps emblematic of the broader uncertainties characterizing the Chinese e-commerce domain.

The Road Ahead: Price Targets and Projections

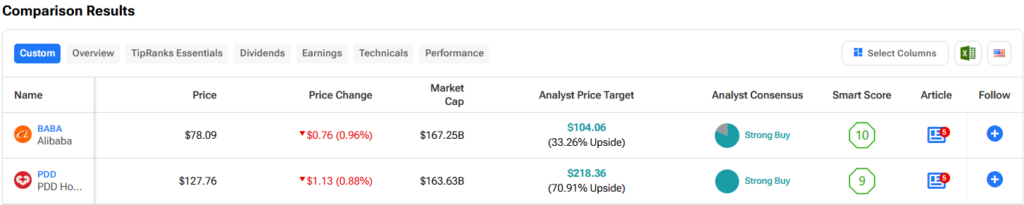

Alibaba’s price trajectory, buoyed by a Strong Buy consensus rating underpinned by 13 Buy, three Hold, and zero Sell ratings, unfurls a compelling narrative of a 33.5% upside potential at an average stock price of $104.06.

Conversely, PDD’s enigmatic trajectory mirrors its operational Decalogue, navigating a realm governed by regulatory nuances and growth mandates. The confluence of regulatory challenges, financial transparency imperatives, and growth aspirations herald a tempestuous yet captivating journey for investors treading the path of Chinese e-commerce giants.

Unpacking the Future: Chinese Giants Alibaba and PDD Holdings Unraveled

The Potential of PDD Stock

With its share price tagged at an appetizing $218.36, analysts have labeled PDD Holdings with a resounding Strong Buy consensus rating. Over the past three months, investors have offered up 13 Buys, zero Holds, and zero Sells. This bullish sentiment hints at a promising upside potential of 70.8% for those willing to take the plunge. It seems there’s more than meets the eye with PDD.

Deciphering the Investment Landscape

Perched at the crossroads of financial intricacies and market volatilities, Alibaba and PDD dominate the realm of Chinese stocks. While both companies exude allure for the steadfast investor, Alibaba emerges as the brighter star in this celestial alignment. Traders and analysts alike point to concerns over the ebb and flow of consumer spending in China as a damper on both entities. Yet, these clouds are but fleeting shadows on the horizon, hinting at an opportune moment to seize the reins and ride the profits that may follow.

A looming specter of delisting hangs over Chinese stocks on U.S. exchanges, a risk apparent to both titans of commerce. PDD, however, courts a more precarious position, shackled to the potential fallout from U.S. legislative muscle aimed at TikTok. In this delicate dance of politics and power struggles, Alibaba emerges as the stouter contender, a bastion of stability in the tumultuous sea of e-commerce. Alibaba beckons as the anchor, a safe harbor amidst the swirling tempest.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.