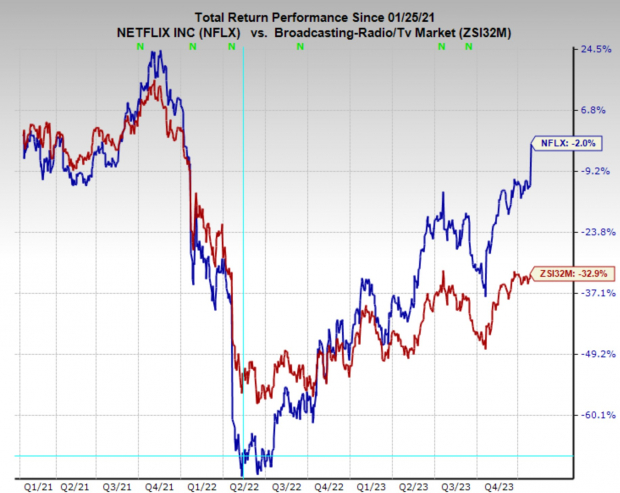

Netflix’s stock has surged more than 10% today following its recent earnings report, marking an impressive comeback after a drastic 75% drop from its all-time high in 2022. This resurgence is a testament to its dominance in the online content industry, with the stock nearly tripling from its lows and reaching two-year highs.

During the earnings call, Netflix displayed robust growth in subscribers and revenue, outlining a long-term strategy to diversify its content offerings. The company’s Zacks Rank #2 (Buy) rating further underscores its positive outlook for investors.

Image Source: Zacks Investment Research

An Upbeat Earnings Call

Netflix reported strong Q4 2023 results, with a notable 12% year-over-year revenue growth that surpassed expectations. The company’s operating margins improved to 21%, exceeding the targeted 20%. It also achieved a significant increase in free cash flow, reaching $6.9 billion for the year.

Furthermore, Netflix unveiled plans to venture into diverse content types, including games, live programming, and sports-related content, along with scaling its advertising business to enhance user engagement.

In Q4 2023, Netflix added 13.1 million paid subscribers, setting a new record with 260.8 million paid subscribers in total. The quarter also saw a 12% revenue growth, driven by pricing adjustments, strong content offerings, and the benefits of paid sharing. The company’s operating income for Q4 reached $1.5 billion, a substantial increase from the previous year, leading to an operating margin of 17%. For the entire 2023 fiscal year, Netflix generated $7 billion in operating income, surpassing expectations and achieving an operating margin of 21%.

Despite a slightly lower-than-projected EPS of $2.11 for Q4, Netflix expressed optimism for 2024, predicting healthy double-digit revenue growth and raising the full-year operating margin outlook from 22-23% to 24%. The company aims to sustain robust revenue growth, expand operating margins, and further increase free cash flow. In an effort to stay competitive in the streaming market, Netflix emphasized its commitment to continuous improvement, innovation, and substantial investments in content, advertising, and games.

Netflix believes it has significant room for growth, currently representing only about 5% of the $600 billion-plus revenue market across paid TV, film, games, and branded advertising.

Intense Competition

In the fiercely competitive streaming landscape, Netflix faces formidable rivals such as Amazon, Disney, Alphabet, and Apple. The company’s remarkable growth this quarter is a testament to its resilience and market leadership, particularly in the face of such stiff competition.

While these tech giants have diversified business portfolios, Netflix’s unwavering focus on streaming shows its ability to thrive in an industry where specialization is key. Comparison with the upcoming earnings releases from Alphabet, Apple, and Amazon will provide valuable insights into the performance of each player within the market.

The Bottom Line

Despite the substantial share price appreciation, Netflix remains a compelling investment option. The company’s impressive revenue and subscriber growth, expanding margins and profits, and its foray into new entertainment avenues, all contribute to its appealing prospects. Furthermore, Netflix is currently trading at a relatively inexpensive valuation, presenting an attractive opportunity for investors.

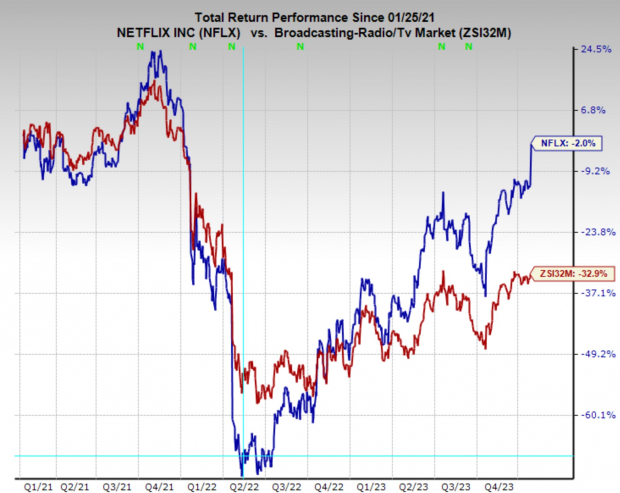

Image Source: Zacks Investment Research

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.