Key Points

-

Over the last few weeks, other players in big tech reported their latest quarterly results.

-

One major theme from those reports is that hyperscalers are accelerating their AI infrastructure spending.

-

That build-out will prove a multiyear, multitrillion-dollar catalyst for data center chip companies like Nvidia.

- 10 stocks we like better than Nvidia ›

Nvidia (NASDAQ: NVDA) stands at the center of the artificial intelligence (AI) revolution, and the company’s upcoming earnings report on May 20 has investors buzzing. With the stock having delivered generational returns over the last few years, you might be wondering whether to add shares ahead of the print or wait for the results.

The data we already have offers a compelling case for buying now — not because of short-term timing strategies, but rather because of durable secular tailwinds and a valuation that still offers a reasonable entry point for those seeking long-term upside.

Will AI create the world’s first trillionaire? Our team just released a report on the one little-known company, called an “Indispensable Monopoly” providing the critical technology Nvidia and Intel both need. Continue »

While Wall Street’s consensus sets a high bar, based on Nvidia’s various catalysts, the company looks poised to clear it. Meanwhile, history and valuation reinforce the case for action over hesitation.

![]()

Image source: Nvidia.

What are Wall Street’s expectations for Nvidia’s Q1 results?

According to data compiled by Yahoo! Finance, Wall Street analysts expect Nvidia to deliver $78.8 billion in revenue and $1.77 in earnings per share (EPS) for the quarter. These figures are in line with management’s own guidance from the prior quarter, which pointed to $78 billion in sales excluding any business from China.

Several powerful catalysts support its chances of meeting — or exceeding — these targets. First, AI hyperscalers dramatically raised their capital expenditure plans after delivering their own first-quarter results. Microsoft, Amazon, Alphabet, and Meta Platforms collectively signaled spending of approximately $725 billion in 2026, a roughly 77% increase from 2025.

These increases stem from accelerated data center buildouts to support large language model (LLM) training and real-time inference deployments. In addition, higher component costs and capacity constraints have reinforced big tech’s collective decision to double down on infrastructure. Executives at each of these companies have emphasized that AI infrastructure remains capacity-limited, not demand-limited.

This type of environment is a direct bellwether to Nvidia, whose GPUs and networking solutions serve as the backbone of hyperscale chip clusters. In my view, the real focus from Wall Street when the report comes out will be on Nvidia’s guidance. Any commentary suggesting sustained, high-double-digit percentage revenue growth through the year would validate the AI capex supercycle and likely lift sentiment.

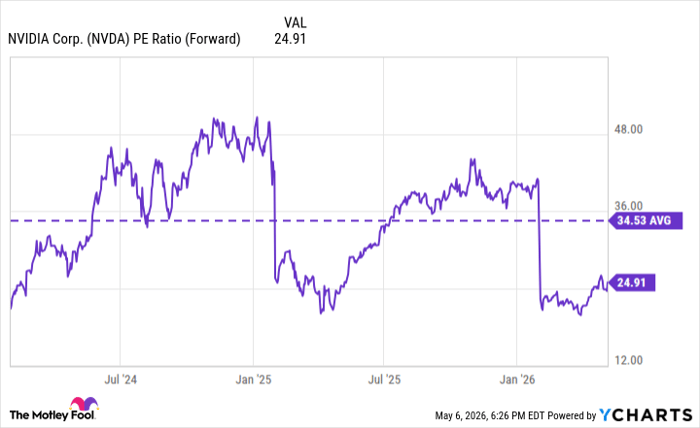

Nvidia’s valuation points to a buy-and-hold strategy

Currently, Nvidia trades at a forward price-to-earnings (P/E) multiple of 25 — well below its average during the AI revolution. When viewed against the scale of the AI opportunity — trillions of dollars in potential infrastructure spending over the coming decade — Nvidia’s valuation appears quite reasonable rather than stretched for a secular compounder.

NVDA PE Ratio (Forward) data by YCharts.

Attempting to time the market around a single earnings event is usually an exercise in false precision. Macroeconomic uncertainties and sentiment swings may create temporary selling pressure, but these influences have always proved fleeting. The smarter approach is to focus on the long-term fundamentals: Nvidia’s dominant market position, accelerating product cycles, and the shift toward AI across industries beyond technology.

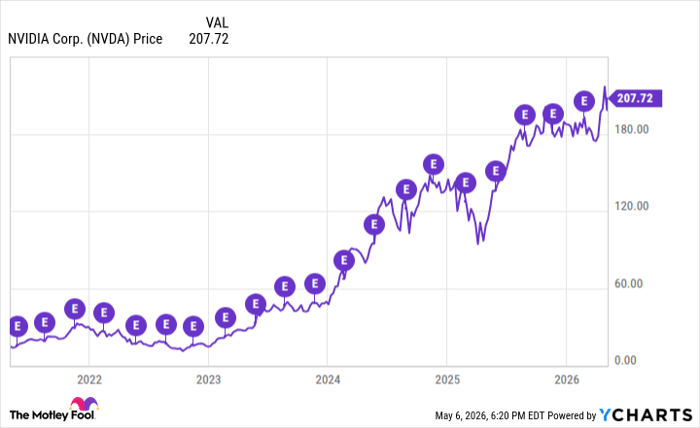

How does Nvidia stock typically move following an earnings report?

Nvidia’s track record following an earnings report offers another layer of insight for smart investors. Throughout the AI revolution, the company has beaten consensus estimates most of the time.

As the chart above reflects, the short-term stock reactions to those reports are usually modest — Nvidia shares tend to post small gains in the first day or week after the print becomes public knowledge. Yet the longer-term picture offers a more decisive conclusion.

Holding Nvidia stock through earnings has historically rewarded investors handsomely. Average returns one quarter later tend to rise by double digits, while one-year returns have frequently exceeded 100% during more bullish cycles. This pattern suggests that while volatility often spikes on or around report day, the underlying trend favors those who buy and hold the stock while looking past the noise.

At the end of the day, earnings reports have ultimately served more as confirmation of Nvidia’s dominance in the AI realm than as signals of inflection risks. Therefore, history would advise against emotional pre-earnings selling or waiting on the sidelines. Buying more Nvidia stock during pre-earnings dips will likely pay off through the multiquarter compounding that generally follows strong results and guidance.

Should you buy stock in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $471,827!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,319,291!*

Now, it’s worth noting Stock Advisor’s total average return is 986% — a market-crushing outperformance compared to 207% for the S&P 500. Don’t miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of May 10, 2026.

Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has a disclosure policy.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.