Advanced Micro Devices (NASDAQ: AMD) has experienced a considerable pullback of nearly 15% from its peak of $227 per share in early March. This correction presents a unique conundrum for investors eyeing the AI market, given AMD’s surging valuation and the recent market turbulence. As the dust settles on this correction, investors find themselves at a crossroads – to either seize this dip as a strategic buying opportunity or exercise caution and remain on the sidelines.

Exploring AMD’s Current Position

Despite the recent market corrections, AMD’s stock price has soared by approximately 85% in the past year. This meteoric rise can be partly attributed to the heightened interest in its AI chip portfolio, particularly the Instinct MI300 Series Accelerators. While AMD competes with industry behemoth Nvidia (NASDAQ: NVDA) for market share, forecasts by MarketDigits predict a robust 38% compound annual growth rate for the AI chip market till 2030. This favorable market trend has allowed AMD to flourish even with a modest market share.

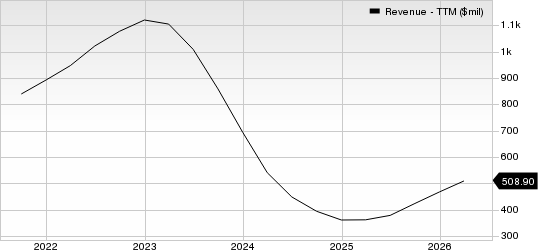

Financially, AMD has demonstrated resilience. In the fourth quarter of 2023, its revenue climbed 10% year-over-year to reach $6.2 billion. Notably, the data center segment, inclusive of AI chips contributing $2.3 billion, witnessed a remarkable 38% annual growth. Additionally, the client segment showcased impressive growth with a 62% revenue surge year-over-year to $1.5 billion. These positive metrics underscore AMD’s strong performance across various business segments, countering declines in gaming and embedded sectors.

While AMD refrained from issuing full-year guidance for 2024, analysts are optimistic, projecting a 23% revenue growth for the current year and a further 26% surge in 2025. Such promising growth trajectories are anticipated to propel net income substantially, potentially boosting the stock price over the long term.

AMD’s Ongoing Challenges

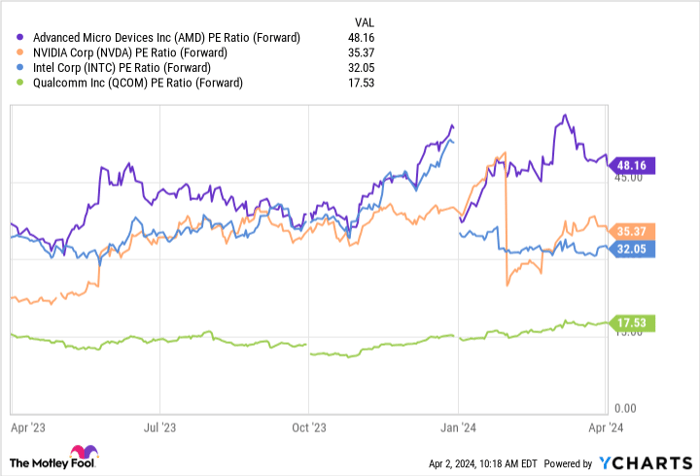

However, AMD’s financials also bear the brunt of industry cyclicality. Its revenue for 2023 slipped by 4% to $23 billion, with growth only observed in the data center and embedded segments. This decline in operational performance resulted in a significant drop in operating income, with net income plunging by 22% to $4.3 million. Furthermore, AMD’s sky-high price-to-earnings (P/E) ratio, currently hovering around 350, appears more reflective of profit declines rather than offering a true reflection of its valuation. Even its forward P/E ratio of 48 raises concerns about the stock’s steep pricing.

Comparatively, AMD’s valuation pales in comparison to industry players like Intel (NASDAQ: INTC) and Qualcomm (NASDAQ: QCOM) who have also made significant strides in AI-ready chip development. The sizable gap between AMD’s forward P/E ratio and that of market leader Nvidia may exert pressure on potential gains, potentially stalling or reversing positive momentum over time.

Seizing the Correction – A Wise Move?

Against the backdrop of the burgeoning AI chip market, purchasing AMD stock appears prudent. As the company bolsters its chip offerings to meet market demand, a consequent upsurge in revenue and income seems foreseeable. The encouraging performance in the fourth quarter signals the initiation of this upward trajectory.

While AMD’s valuation looks stretched compared to rivals like Nvidia and emerging AI players, the substantial growth outlook for the AI chip market hints at a rising tide that may lift all semiconductor boats. Coupled with AMD’s diversified business segments, the recent stock pullback might indeed represent an opportune moment for investors to delve into this semiconductor stock rather than adopting a cautious stance.

5 Stocks Our Experts Predict Could Double In the Next Year

By submitting your email, you'll also get a free pivot & flow membership. A free daily market overview. You can unsubscribe at any time.